Fifth Circuit Review—Reviewed: Reports of Auer’s Death Are Greatly Exaggerated

Welcome back to another edition of Fifth Circuit Review—Reviewed! I have several noteworthy cases to report on, including the Fifth Circuit’s first full-blown application of the five-part test from Kisor v. Wilkie, 139 S. Ct. 2400 (2019). Let’s dig in.

Auer Deference Alive and Well in Fifth Circuit Post-Kisor

Johnson v. BOKF National Association, No. 18-11375 (5th Cir. Sept. 29, 2021) (Higginbotham, Dennis, JJ.) (Ho, J., concurring in judgment only)

At long last, the Fifth Circuit has applied the new Auer deference framework established over two years ago in Kisor. The question in Johnson v. BOKF, National Association was whether a national bank had violated the National Bank Act of 1864 by charging its checking account customers “extended overdraft charges.” The Act limits the rate of “interest” national banks may charge on a “loan.” 12 U.S.C. § 85. Sharonda Johnson claimed the Bank violated the act when it charged her for failing to reimburse the Bank for covering her overdraft of her checking account. Johnson argued that

- When the Bank chose to cover her overdraft, it made her a “loan” for section 85 purposes;

- The fee the Bank imposed when Johnson failed to repay that “loan” on time was “interest” under the Act; and

- Because that “interest” charge exceeded the statutory limit, the Bank violated section 85 by imposing it.

The district court rejected Johnson’s premises and dismissed her case for failure to state a claim. The Fifth Circuit affirmed. Judge Dennis’s opinion for the court, which Judge Higginbotham joined, agreed with the district court that the Bank’s extended overdraft charges are not “interest” under the Act. In so holding, the panel deferred to a 2007 Interpretive Letter from the Office of the Comptroller of Currency–the federal agency tasked with implementing the statute. Judge Ho concurred in the judgment only. In a departure from his usual habit, however, Judge Ho didn’t write separately to explain his reasoning for doing so.

The 2007 Interpretive Letter in Context

Some regulatory history is essential here. OCC regulations distinguish “interest” charges from non-interest “account services” charges. See 12 C.F.R. § 7.4001(a) (defining “interest”); id. § 7.4002(a) (“A national bank may charge its customers non-interest charges and fees, including deposit account service charges.”). In 2001, OCC acknowledged that its regulations did not address whether interest includes “at least some portion of the fee imposed by a national bank when it pays a check notwithstanding that its customer’s account contains insufficient funds to cover the check.” Recognizing that “[a] bank that pays a check drawn against insufficient funds may be viewed as having extended credit to the accountholder,” OCC opened the issue to public comment in 2001. After reviewing “numerous comments,” OCC concluded the issue was “complex and fact-specific” and declined to amend its regulations to address it.

That brings us to the 2007 Interpretive Letter that proved decisive in this case. OCC wrote the letter in response to a national bank in California that had requested confirmation that its approach to charging and recovering overdraft fees complied with the statute and OCC’s regulations. The bank was facing two lawsuits challenging its practice of recouping overdrafts and related fees from public benefits payments the bank’s customers had deposited in the overdrafted accounts. Its letter to OCC “describe[d] in some detail the [b]ank’s process for honoring and clearing overdraft items.” OCC’s response condensed that detail into a one-paragraph summary. In a footnote, OCC mentioned that the bank imposed a “Continuous Overdraft Charge” similar to BOKF’s extended overdraft charges.

OCC confirmed that the bank’s policies complied with the Act and the agency’s regulations. It emphasized that “[t]he process by which a bank honors overdraft items is typically part of the Bank’s administration of a depositor’s account,” and “[c]reating and recovering overdrafts have long been recognized as elements of [account services] that banks provide.”

Notably, however, the Interpretive Letter does not mention

- section 7.4001(a);

- OCC’s 2001 claim that interest may include “at least some portion of the fee imposed by a national bank when it pays a check notwithstanding that its customer’s account contains insufficient funds to cover the check”;

- OCC’s 2001 recognition that “[a] bank that pays a check drawn against insufficient funds may be viewed as having extended credit to the accountholder”; or

- OCC’s 2001 conclusion after notice and comment that the question is too complex and fact specific to resolve by regulation.

After surveying this same history, Judge Dennis framed the panel majority’s task:

We must decide, then, whether OCC’s conclusion that these sort of Extended Overdraft Charges are a “deposit account service charge[ ]” under 12 C.F.R. § 7.4002(a), and therefore not interest under § 7.4001(a), is entitled to deference.

Applying the Kisor Framework

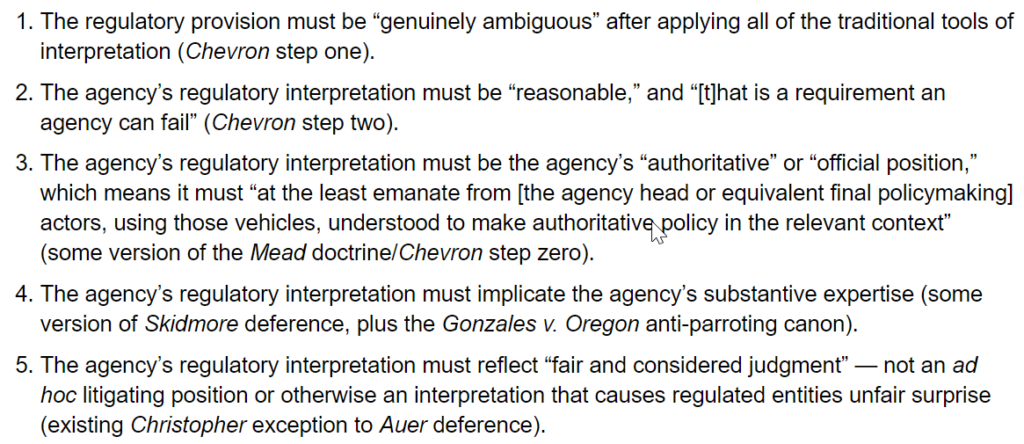

As Chris Walker explained here, the Kisor framework has five steps:

I summarize and critique the majority’s reasoning at each step below.

Step 1

The majority concluded that the regulations are genuinely ambiguous because OCC

- has described them as ambiguous, and

- decided not to amend them in 2001, reasoning that whether interest includes any portion of the fee imposed by a national bank when it pays a check drawn on insufficient funds implicates “complex and fact-specific concerns.”

I don’t find those reasons especially convincing. The first is arguably at odds with Kisor‘s instruction that courts should conduct the step-one inquiry on their own and as “if [they] had no agency to fall back on.” The second strikes me as irrelevant. After all, it’s not as though outcomes under unambiguous standards cannot hinge on “fact specific” considerations.

What concerns me most about the majority’s step-one analysis, however, is its failure to engage meaningfully with the text. Compare the majority’s discussion in this case with, for example, the Ninth Circuit’s inaugural application of Kisor in Amazon.com v. IRS, which William Yeatman discussed in detail here. While the majority may well have reached the correct result in this case, I wish it would have “empt[ied] the judicial toolkit” before “waving the ambiguity flag.”

Step 2

The majority concluded that OCC’s interpretation is reasonable because (1) Johnson doesn’t contend otherwise and (2) it “is consonant with the majority view on the subject based on the public comment submissions” OCC received during the 2001 rulemaking.

I’m skeptical of comment counting as a metric of reasonableness. For one thing, it’s too easy for spam comments, form comments, and fraudulent comments to skew the numbers. For another, there is no guarantee that any–much less every–public commenter cares whether his or her favored interpretation is a permissible construction of the regulation.

Step 3

The majority concluded that the 2007 Interpretive Letter represents the agency’s authoritative and official position because

- it was drafted by a senior OCC official;

- it was written in response to a request for guidance under the National Bank Act and the agency’s regulations; and

- the bank requesting the guidance specifically asked about charges like those at issue in Johnson’s case, and OCC concluded that they are non-interest account services charges.

A couple of comments regarding points 2 and 3. It is true that OCC wrote the 2007 Interpretive Letter in response to a request for guidance under the National Bank Act and the agency’s regulations. And it is also true that courts have deferred to OCC interpretive letters in the past. In my view, however, the “character and context” of this letter arguably requires a different conclusion. When OCC considered addressing this issue directly in 2001, it chose to do so through notice-and-comment rulemaking. The fact that the agency used a less formal process–providing guidance to a regulated party through a letter not published in the Federal Register–when issuing the 2007 Interpretive Letter makes me wonder whether the letter reflects OCC’s official and authoritative position on the issue.

As for Judge Dennis’s final point–that OCC expressly addressed charges like those at issue in Johnson’s case in the 2007 Interpretive Letter–that was not at all obvious to me after reading the letter. As I explained in the discussion of the regulatory history above, the letter mentions the charges at issue only once in a footnote, and it doesn’t discuss § 7.4001(a) at all. Judge Dennis is right that OCC’s description of the requesting bank’s charges as account services charges is categorical. But because the interest issue in Johnson’s case–the one OCC declined to address in 2001–was not before the agency when it wrote the 2007 Interpretive Letter, I’m less convinced it intended to announce a departure from its 2001 position on the question.

Step 4

The majority concluded that the “OCC’s interpretation of §§ 7.4001(a) and 7.4002 also falls squarely within the agency’s substantive expertise” because “OCC is administering the NBA and regulations promulgated thereunder.”

That may prove that OCC has expertise, but I read Kisor as requiring courts to ask whether the agency “us[ed] its expertise and experience to formulate [the interpretation at issue].” That distinction might make no difference to the majority in Johnson’s case, but it strikes me as important for purposes of nailing down the standard for future cases.

Step 5

The majority concluded that the 2007 Interpretive Letter reflects OCC’s fair and considered judgment because:

- there is “no indication that the interpretive letter was merely a ‘convenient litigating position’ or ‘post hoc rationalization advanced to defend past agency action against attack,'” and

- Johnson doesn’t contend that it “creates unfair surprise to regulated parties.”

Fair enough, but I wish the majority would have addressed OCC’s departure from the position it took in the 2001 rulemaking. After all, Kisor warns that deference to an agency construction “conflict[ing] with a prior” one should be given “only rarely.”

Judge Ho’s View of the Case

Judge Ho concurred in the judgment only, but he didn’t write separately to explain his view of the case. My guess is that he either (1) believes that the text of the regulations (or statute?) unambiguously excludes the charges at issue from the definition of “interest” or (2) would have affirmed on the district court’s other ground for dismissing Johnson’s claim: that a bank does not make a “loan” to its checking account customer for purposes of the National Bank Act when it elects to cover an overdraft. The majority doesn’t address the “loan” question at all.

Supreme Court to Consider Overruling 1994 Fifth Circuit Decision at the Heart of Decades-Long Feud Over Indian Gaming

The Supreme Court recently granted review in Ysleta del Sur Pueblo v. Texas, the latest case in a longstanding dispute over the application of Texas law to tribal gaming operations on Native American land. The case involves a federal law that bars on tribal lands any gaming activities “prohibited by the laws of the State of Texas.” The question is whether the law prohibits any kind of gambling that is banned under state law, or whether it also prohibits any gaming that the state regulates. Petitioners are asking the Court to overrule the Fifth Circuit’s 1994 decision in Ysleta del Sur Pueblo v. Texas, 36 F.3d 1325 (5th Cir. 1994), which held that Texas gaming laws and regulations operate as surrogate federal law on the Ysleta del Sur Pueblo’s reservation in Texas.

Panel Divides Over Reviewability of APA Claim Against HUD

Hawkins v. HUD, No. 20-20281 (5th Cir. Oct. 13, 2021) (Wiener, Dennis, JJ.) (Duncan, J., dissenting)

Tenants living in substandard conditions in a “Section 8” housing project in Houston sought relocation assistance vouchers from HUD. When HUD failed to oblige, the tenants sued to compel the agency to provide the vouchers. The district court concluded that HUD’s decision (1) was committed to agency discretion by law (2) was not final agency action subject to APA review.

A divided Fifth Circuit panel reversed. Judge Dennis joined Judge Wiener’s majority opinion holding that HUD’s own regulations obligated it to provide vouchers “if … the family wishes to be rehoused in another dwelling unit.” 24 C.F.R. § 886.323(e). And because the tenants had alleged that HUD’s failure to provide the vouchers was the consummation of the agency’s decision-making process, the district court had erred in concluding that they had not alleged final agency action.

Judge Duncan dissented. His primary concern was that the majority’s holding upset decades of settled agency practice under the regulation at issue. As for final agency action, Judge Duncan insisted that the majority “conjure[d] [it] out of thin air.” In his view, the mere fact that HUD had the authority to issue vouchers but had not done so yet didn’t mean the agency had concluded once and for all that vouchers were out of the question.

Panel Holds Niz-Chavez v. Garland, 141 S. Ct. 1474 (2021) Governs Notice Requirements Applicable to In Absentia Removal

Rodriguez v. Garland, No. 20-60008 (5th Cir. Sept. 27, 2021) (Higginbotham, Willett, Duncan)

In Rodriguez, the court held that although Niz-Chavez focused on the stop-time rule, the Supreme Court “interpreted [8 U.S.C.] § 1229(a) separately from the stop-time statute” in holding that § 1229(a) requires a written notice containing all the required information. Because “[b]oth th recission of an in absentia order provision and the stop-time rule provision specifically reference the § 1229(a) notice requirements,” the panel reasoned, Niz-Chavez “applies in the in absentia context as well.” The panel emphasized that “[t]he specific textual reference to § 1229(a) distinguishes these provisions from others we have considered, including § 1227(a)(2)(A) at issue in Maniar v. Garland.”

See ya next time!