Crypto Litigation: An Empirical View

PDF DownloadCrypto assets and the crypto-asset ecosystem have introduced novel legal challenges, many of which have reached the United States judicial system. In this Essay, I offer the first empirical analysis of all crypto-related cases litigated in the United States, analyzing the number of cases, types of disputes, and causes of actions, among other criteria. The novel and carefully hand-coded dataset includes all cases involving crypto assets and the related ecosystem including cryptocurrencies, tokens, exchanges, and decentralized autonomous organizations (DAO). Using this dataset, I show that crypto litigation to date has been dominated by securities litigation and associated tort claims. However, using recent examples, I predict that future cases will involve more nuanced and complex private law analyses of crypto assets. In sum, I argue that the United States is at a turning point in crypto litigation, which I call the “private law pivot.” The private law pivot presents novel queries to the courts stemming from contract law and business formation issues.

Introduction

In the early part of 2022, as cryptocurrencies crashed in value, lawsuits related to crypto assets soared. It is estimated that as of May 2022, more than 200 individual and class action lawsuits have been filed—up 50% since the start of 2020.11.Sam Skolnik, Crypto Lawsuit Deluge Has Big Firms Scrambling to Keep Up, Bloomberg Law (May 17, 2022), https://news.bloomberglaw.com/business-and-practice/crypto-lawsuit-explosion-has-big-law-scrambling-to-keep-up (https://perma.cc/8P8Z-NC6S). As the total value destroyed in the current crypto wipeout passes $2 trillion, one can only expect more disputes to arise.22.MacKenzie Sigalos, Why the $2 Trillion Crypto Market Crash Won’t Kill the Economy, CNBC (June 19, 2022), https://www.cnbc.com/2022/06/18/why-the-2-trillion-crypto-market-crash-wont-kill-the-economy.html (https://perma.cc/HV6K-SXN7). By way of comparison, in 2008 alone, during the height of the financial crisis, close to 560 cases, including 91 federal securities class actions, were filed.33.The Financial Crisis 10 Years Later: Lessons Learned, Paul, Weiss LLP (Sept. 15, 2018), https://www.paulweiss.com/practices/litigation/financial-institutions/publications/the-financial-crisis-10-years-later-lessons-learned?id=27324 (https://perma.cc/UQK8-NCQT). The financial crisis left a lasting impact on the economy, and its aftershocks continue to be felt in the judiciary thirteen years later, with the U.S. Supreme Court recently ruling on a related securities class action.44.See, e.g., Goldman Sachs Group, Inc. v. Arkansas Teacher Retirement System, 141 S. Ct. 1951 (2021).

Crypto’s ongoing meltdown, or, as an enthusiast would call it, “crypto winter,” will most likely lead to a similar cascade of lawsuits. To provide a glimpse of the magnitude of the crash, over the course of just three months, a token named Luna collapsed, eradicating more than $80 billion of value. Two crypto brokers and exchanges, Celsius and Voyager, and a crypto hedge fund named Three Arrows Capital have declared bankruptcy—a series of failures that has been compared to the downfall of the Lehman Brothers.55.MacKenzie Sigalos, From $25 Billion to $167 Million: How a Major Crypto Lender Collapsed and Dragged Many Investors Down with It, CNBC (July 18, 2022), https://www.cnbc.com/2022/07/17/how-the-fall-of-celsius-dragged-down-crypto-investors.html (https://perma.cc/UQK8-NCQT).

Most recently, FTX, one of the world’s largest cryptocurrency exchanges, collapsed in a matter of days. The stunning series of events closely resembled a classic bank run—with some novel twists. A document was leaked that suggested a hedge fund closely related to FTX leveraged FTX’s tokens, FTT, as collateral for its speculative investments. This revelation resulted in the decision of Binance, FTX’s major competitor, to sell all of its FTT tokens. Binance’s move precipitated massive withdrawal requests that FTX was unable to fulfill.66.Kalley Huang, Why Did FTX Collapse? Here’s What We Know., N.Y. Times (Nov. 18, 2022), https://www.nytimes.com/2022/11/10/technology/ftx-binance-crypto-explained.html (https://perma.cc/7KKK-8MXU). This story is still developing, but the fallout from FTX has already led to a bankruptcy proceeding in Delaware and a class-action lawsuit against celebrity promoters—including Larry David, Tom Brady, Giselle Bündchen, Shaquille O’Neal, and Stephen Curry—in the hope of recovering (some of) the $32 billion of wealth wiped out as a resulted of FTX’s collapse.77.David Yaffe-Bellany, FTX Assets Still Missing as Firm Begins Bankruptcy Process, N.Y. Times (Nov. 22, 2022), https://www.nytimes.com/2022/11/22/business/ftx-bankruptcy-sam-bankman-fried.html (https://perma.cc/9PNZ-K5VT); Zoe Guy, Celebrity Crypto Ambassadors Sued Over FTX Crash, Vulture (Nov. 17, 2022), https://www.vulture.com/2022/11/ftx-lawsuit-celebrities.html (https://perma.cc/DXS9-YK8G).

Despite experiencing a massive valuation at its peak (roughly $3 trillion dollars in November of 2021),88.Yvonne Lau, Cryptocurrencies Hit Market Cap of $3 Trillion For the First Time as Bitcoin and Ether Reach Record Highs, Fortune (Nov. 8, 2021), https://fortune.com/2021/11/09/cryptocurrency-market-cap-3-trillion-bitcion-ether-shiba-inu (https://perma.cc/QG3A-5UVU). the crypto landscape is a virtual no man’s land. Put differently, the cryptocurrency market is largely unregulated. The growing chorus of calls for regulation, including from key crypto players themselves, is a testament to this reality and indicates the urgency of a policy response.99. Benjamin Powers, Why the Crypto Crash is Fueling Calls for Regulation, Grid (June 27, 2022), https://www.grid.news/story/technology/2022/06/27/why-the-crypto-crash-is-fueling-calls-for-regulation/ (https://perma.cc/R2TW-UZ3B). Regulating cryptocurrencies is undoubtedly challenging as the crypto landscape is evolving and regulating it requires a deep understanding of novel technologies and concepts, such as decentralized finance,1010. Decentralized Finance (DeFi) aims to provide traditional financial services such as lending, loans, interest, and deposits using distributed networks with the goal of disintermediating the banks (peer-to-peer lending, for example). See James Royal & Brian Beers, What is DeFi? A beginner’s guide to decentralized finance, Bankrate (April 15, 2022), https://www.bankrate.com/investing/what-is-decentralized-finance-defi-crypto (https://perma.cc/JR9E-DWYE). smart contracts,1111. Smart contracts refer to automatic (and predetermined) conditions (and obligations) that are distributed and can function like apps in a centralized system. See Farshad Ghodoosi, Contracting in the Age of Smart Contracts, 96 Wash. L. Rev. 51, 58-64 (2021); see also What are smart contracts on blockchain?, IBM, https://www.ibm.com/topics/smart-contracts (https://perma.cc/U7KD-KL2Z). oracles,1212. Oracles are the links between smart contracts and the real world. Smart contracts rely on oracles to receive information from the real world. Guilio Caldarelli, Understanding the Blockchain Oracle Problem: A Call for Action, MDPI (Oct. 29, 2020), https://www.mdpi.com/2078-2489/11/11/509/htm (https://perma.cc/RF5D-WE7U). decentralized autonomous organizations (DAO),1313. A DAO is a distributed organization built on smart contracts and blockchain that aims to enable decentralized organizational decision-making. Part of DAO’s promise is to shift organizational decision-making to stakeholders. See Farshad Ghodoosi & Monica Sharif, The Ethics of Blockchain in Organization, 178 J. Bus. Ethics, 1009, 1012 (2022). See generally S. Wang, et al., Decentralized Autonomous Organizations: Concept, Model, and Applications, 6 IEEE Transactions on Computational Soc. Sys. 870 (2019). Web 3.0,1414. Web 3.0 is in its inception and refers to the world wide web that is interactive, equipped with AI, and decentralized. Riaan Rudman & Rikus Bruwer, Defining Web 3.0: Opportunities and Challenges, Emerald Insight (Feb. 1, 2016), https://doi.org/10.1108/EL-08-2014-0140 (https://perma.cc/W9U6-J58A). algorithmic stablecoins,1515. The value of stablecoins is often pegged to a certain currency, like the U.S. Dollar. James Royal & Brian Beers, What are Stablecoins and How Do They Affect the Cryptocurrency Market?, Bankrate (May 12, 2022), https://www.bankrate.com/investing/stablecoin-cryptocurrency/ (https://perma.cc/4FMC-QHNB). NFTs,1616. Non-fungible tokens, or NFTs, refer to digital arts on the Ethereum blockchain that are unique. Mitchell Clark, NFTs, Explained, The Verge (June 6, 2022), https://www.theverge.com/22310188/nft-explainer-what-is-blockchain-crypto-art-faq (https://perma.cc/5LJZ-NFJ). proof of work,1717. Proof of work refers to the verification of transactions in a distributed network that is based on participants who validate incoming transactions while receiving some tokens as rewards for their validation. E. Napoletano & Benjamin Curry, Proof of Work Explained, Forbes (Apr. 8, 2022), https://www.forbes.com/advisor/investing/cryptocurrency/proof-of-work/ (https://perma.cc/EUY8-8X64). proof of stake,1818. Proof of stake refers to the verification of transactions in a distributed network that is based on select number of “validators.” E. Napoletano & Benjamin Curry, Proof of Stake Explained, Forbes (Apr. 8, 2022), https://www.forbes.com/advisor/investing/cryptocurrency/proof-of-stake/ (https:// perma.cc/JA7L-XBLU). tokens,1919. Tokens are a representation of a medium of exchange (or a real asset) which can be traded, held for value, or staked (virtually deposited) to earn interest. Lyle Daly, What Are Crypto Tokens?, The Motley Fool (June 27, 2022), https://www.fool.com/investing/stock-market/market-sectors/financials/cryptocurrency-stocks/crypto-tokens/ (https://perma.cc/TZ7G-4L2J). decentralized exchanges,2020. A decentralized exchange, as opposed to traditional exchange, facilitates peer-to-peer trading with no involvement by intermediaries. What is a DEX?, Coinbase, https://www.coinbase.com/learn/crypto-basics/what-is-a-dex (https://perma.cc/EY7S-45UZ). and, of course, the blockchain.2121. Blockchain is a distributed and immutable ledger for recording data and transactions which are validated by the participants of the network. See What is Blockchain Technology?, IBM, https://www.ibm.com/topics/what-is-blockchain (https://perma.cc/GT44-VRTB). ,2222. The latest calls for regulation emerged in the wake of the $40 billion collapse (de-pegging against the US Dollar) of Luna and TerraUSD, once heralded as the “greatest” algorithmic stable coin ecosystem (project) to date. David Yaffe-Bellany & Erin Griffith, How Trash-Talking Crypto Founder Caused a $40 Billion Crash, N.Y. Times (May 20, 2022), https://www.nytimes.com/2022/05/18/technology/terra-luna-cryptocurrency-do-kwon.html (https://perma.cc/SW5V-P3CZ). The calls for regulation have been renewed following the $32 billion collapse of FTX, with bipartisan efforts to pass the Digital Commodities Consumer Protection Act of 2022. Courtney Degen, FTX bankruptcy draws increased calls for crypto regulation, Pensions & Investments (Nov. 17, 2022), https://www.pionline.com/cryptocurrency/ftx-collapse-draws-increased-calls-cryptocurrency-regulation (https://perma.cc/Y9WU-J4A8). It is worth noting that the recent collapses in the crypto industry have occurred in centralized crypto exchanges, which some argue provides greater support for decentralized exchanges. Michael O’Boyle, FTX Collapse Will Spur Move to Decentralized Exchanges, Franklin’s CEO Says, Bloomberg (Nov. 17, 2022), https://www.bloomberg.com/news/articles/2022-11-17/franklin-ceo-says-ftx-to-spur-move-to-decentralized-exchanges?leadSource=uverify%20wall (https://perma.cc/FB3B-LSAH).

In this Essay, I offer the first empirical analysis of all crypto-related cases litigated in the United States, analyzing the number of cases, types of disputes, and causes of actions, among other criteria. The dataset includes all cases involving crypto assets and the related ecosystem including cryptocurrencies, tokens, exchanges, and DAO. Based on the data, I argue that crypto litigation is undergoing what I call the “private law pivot,” involving fewer securities-offering claims and more independent private law claims arising out of contracts, business formation, and torts.

In Part I, this Essay provides an overview of the database and empirical method. In Part II, the Essay discusses the novel empirical dataset I compiled on private litigation involving crypto assets, dating back to the first case filed in a US court involving crypto assets. It also provides novel data on the causes of actions underlying crypto litigation. In Part III, the Essay considers what the data tell us about the future of litigation in the crypto space.

I. Overview of Empirical Methods

This Essay uses the Morrison Cohen Crypto Litigation Tracker database as the starting point for its empirical analysis. The database “keeps watch on all the latest cryptocurrency and blockchain litigation developments.”2323. Morrison Cohen LLP, Morrison Cohen Cryptocurrency Litigation Tracker (Oct. 4, 2022), https://www.morrisoncohen.com/news-page?itemid=471 (https://perma.cc/PRT6-K2WV). It tracks cases initiated by the Security and Exchange Commission, the Commodity Futures Trading Commission, and the Department of Justice. Additionally, the litigation tracker monitors regulatory proceedings and summary orders, and, importantly for the purposes of this paper, class action suits and other private litigation. By hand coding the data and separately parsing through complaints and related opinions, I created a novel dataset covering the development of private litigation involving crypto assets.

In the process of hand coding, I excluded cases that did not relate directly to privately-owned crypto assets from the dataset. In other words, this Essay analyzed cases in which there were private law issues related to crypto assets that stemmed in whole or in part from contracts or tort. As such, I excluded the following type of cases: bankruptcy cases;2424. See, e.g., In re Cred LLC, No. 20-12836 (Bankr. D. Del. Nov. 7, 2020); In re Cryptopia Ltd., No. 19-11688 (Bankr. S.D.N.Y. May 4, 2019); In re Three Arrows Capital, Ltd., No. 22-10920 (Bankr. S.D.N.Y. July 1, 2022) criminal cases, including those involving the Fourth Amendment;2525. See, e.g., Harper v. IRS, No. 20-cv-00771 (D.N.H. July 15, 2020); Complaint, Blocktree Props., LLC v. Pub. Utility Dist. No. 2 of Grant Cnty., No. 18-cv-390, 2020 WL 1217309 (E.D. Wash. 2018); In re Giga Watt, Inc., No. 18-bk-03197, 2021 WL 321890 (B.A.P. 9th Cir. 2021); Nowak v. Xapo, Inc., No. 20-cv-03643, 2020 WL 5877576 (N.D. Cal. Oct. 2, 2020); Complaint & Demand for Jury Trial, Adler v. Payward, Inc., 2020 WL 5666908 (2d Cir. Sept. 24, 2020); Bitmain v. Doe, No. 18-cv-1626 (W.D. Wash. Nov 8, 2018). employment disputes (typically between crypto firms and their former employees);2626. See, e.g., Complaint, ConsenSys Inc. v. Kavita Gupta, No. 2022-0029 (Del. Ch. Jan 10, 2022); Summons, Kavita Gupta v. Joseph Lubin, ConsenSys Fund I LP, No. 650023/2022 (N.Y. Sup. Ct. Dec. 31, 2021); Summons, Runyon v. Payward, Inc., No. 19-581099 (Cal. Super. Ct. Nov. 26, 2019); Complaint & Demand for Jury Trial, Silverman v. Payward, Inc., No. 19-cv-02997 (S.D.N.Y. Apr. 4, 2019); Complaint & Demand for Jury Trial, Adler v. Payward, Inc., 2020 WL 5666908 (2d Cir. Sept. 24, 2020); Complaint, Wang, Bibox Grou Holdings, Ltd. v. Wei Li, No. 655050/2018 (N.Y. Sup. Ct. Oct. 10, 2018). cyber-attacks and claims against telecommunication companies;2727. See, e.g., Shapiro v. AT&T Mobility, LLC, No. 19-cv-8972 (C.D. Cal. Oct. 17, 2019); Complaint & Demand for Jury Trial, ZG Top Tech. Co. v. John Doe, No. 19-cv-92, (W.D. Wash. Jan. 22, 2019); Complaint, Michael Terpin v. AT&T Inc., No. 18-cv-06975 (C.D. Cal. Aug. 15, 2018). claims against (traditional) banks, including those arising out of The Truth in Lending Act;2828. See, e.g., Complaint & Demand for Jury Trial, Denke v. Citibank, No. 18-cv-4133 (S.D.N.Y. 2018); Complaint & Demand for Jury Trial, Eckhardt v. State Farm Bank, No. 18-cv-01180 (C.D. Ill. May 2, 2018); Complaint & Demand for Jury Trial, Tucker v. Chase Bank, No. 18-cv-03155 (S.D.N.Y. Apr. 10, 2018); Complaint & Demand for Jury Trial, Dunleavy v. Lux Vending, LLC, No. 18-cv-21367 (S.D. Fla. Apr. 6, 2018); Complaint & Demand for Jury Trial, Tapang v. T-Mobile, Inc., No. 18-cv-167 (W.D. Wash. Apr. 4, 2018). insurance claims;2929. See, e.g., Complaint, Kimmelman v. Wayne Ins. Group., No. 18-cv-1041 (Ohio C.P. Feb. 1, 2018). arbitration cases;3030. See, e.g., Morrison Cohen LLP, supra note 23 at 137 (citing claims filed against T-Mobile and AT&T before the American Arbitration Association) See also id. at 156 (citing a similar arbitration claim filed against Payward, Inc.). and patent cases.3131. See, e.g., Complaint & Demand for Jury Trial, Anuwave LLC v. Coinbase, No. 19-cv-1226 (D. Del. June 27, 2019); Complaint & Demand for Jury Trial, Lightwire, LLC v. Zerocoin Electric Coin Company, LLC, No. 19-cv-1292 (D. Colo. May 3, 2019). I also excluded an interpleader case.3232. See Complaint for Interpleader, Bitstamp Ltd. v. Ripple Labs, No. 15-cv-1503 (N.D. Cal. Apr. 1, 2015).

The remaining cases comprised the data which I prepared for empirical analysis. These cases were coded based on the following categories: jurisdiction in which the suit was filed; whether the suit was a class action; and the applicable cause(s) of action. To ensure accurate labeling, the hand-coding process often required a close reading of the pleadings, and if available, court orders and opinions.

The causes of action were divided into (a) contract, (b) tort, (c) securities, (d) consumer protection statutes, (e) trademark, and (f) derivative (fiduciary duty) actions. For coding purposes, contract claims include breach of contract, breach of duty of good faith and fair dealing, unjust enrichment (quasi-contract), and breach of fiduciary duties (other than derivative suits). Tort claims include misrepresentation, fraudulent concealment, fraud in the inducement, and conversion. Securities-based suits include violations of Sections 5, 12, 15, and 17 of the Securities Act3333. 15 U.S.C. § 77e (2018) (prohibiting sale of unregistered securities); 15 U.S.C. § 77l (2018) (imposing civil liabilities for violations of section 77e); 15 U.S.C. § 77o (2018) (setting out liabilities of controlling persons); 15 U.S.C. § 77e (2018) (prohibiting fraudulent transactions in the offer or sale of any securities). and Sections 10(b) and 20 of the Exchange Act,3434. 15 U.S.C. § 78j(b) makes it unlawful to “use or employ, in connection with the purchase or sale of any security” a “manipulative or deceptive device or contrivance in contravention of such rules and regulations as the (SEC) may prescribe.” See also 15 U.S.C. § 78t (2018) (setting out liabilities of controlling persons). along with violations of state securities laws. Consumer protection causes of action include suits brought under statutes such as the California Unfair Competition Law,3535. Cal. Bus. & Prof. Code § 17200 et seq. (West 2022). California Consumer Legal Remedies Act,3636. Cal. Civ. Code § 1750 et seq. (West 2022). and Civil RICO3737. 18 U.S.C. § 1962(a) (2018). See, e.g., Complaint & Demand for Jury Trial, Sorokin v. HDR Global Trading Ltd, No. 21-cv-3576 (N.D. Cal. May 12, 2021). among others. The trademark causes of action refer to allegations arising from Lanham Act’s trademark and false advertising violations.3838. See, e.g., Oracle Corp. v. Crypto Oracle, LLC, No. 19-cv-04900 (N.D. Cal. Feb. 19, 2020); Alibaba Group Holding v. Alibabacoin Foundation, No. 18-CV-2897, 2018 WL 2022626 (S.D.N.Y. 2018); Hermès Int’l v. Rothschild, No. 22-CV-384, 2022 WL 1564597 (S.D.N.Y. 2022). Finally, derivative lawsuit causes of action capture shareholders’ derivative actions against directors and officers for breach of fiduciary duties.3939. See, e.g., Complaint & Demand for Jury Trial, Weathersbee v. Meenavalli, No. 18-cv-10182 (S.D.N.Y. Nov. 11, 2018); Complaint, Hall ex rel. Veritaseum, Inc. v. Middleton, No. 655003/2019 (N.Y. Sup. Ct. Aug. 30, 2019); Complaint & Demand for Jury Trial, Fintz v. O’Rourke, No. 18-cv-9640 (S.D.N.Y., Oct. 22, 2018); Complaint, Rothesay ex rel. Iconic Deo Volente Corp. v. O’Brien, No. 2018-0674 (Del. Ch. Sept. 12, 2018); Summons, Bents ex rel. Longfin Corp. v. Meenavalli No. 653216, (N.Y. Sup. Ct. June 26, 2018); Complaint & Demand for Jury Trial, Hamel ex rel. The Crypto Company v. Poutre, No. 18-cv-616 (C.D. Cal. Jan. 24, 2018).

II. Crypto as Securities Litigation

In this Part, the Essay describes novel data on litigation involving cryptocurrencies to date.

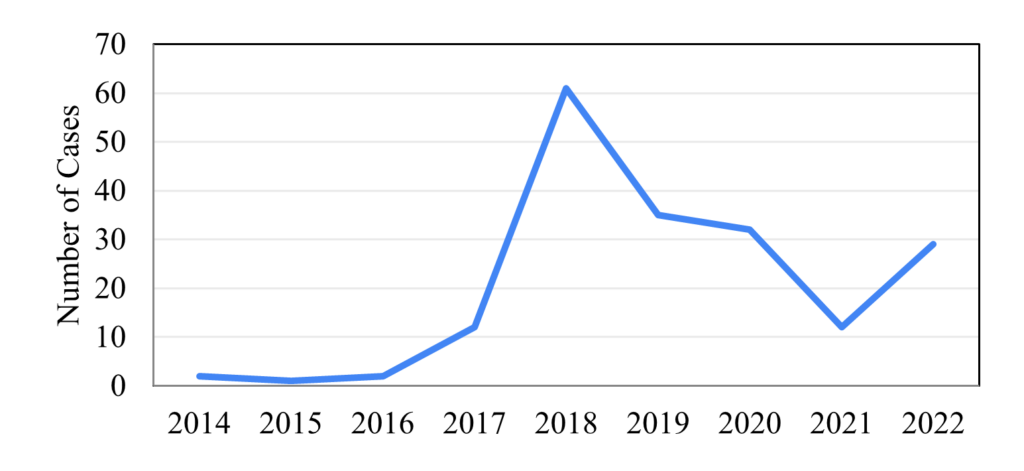

A. Crypto Litigation Peaked in 2018

As a first step, I survey the number of crypto-asset-related cases filed over time. According to the data, the greatest number of court cases related to cryptocurrencies were filed in 2018. One explanation for this peak is that the first “crypto winter”—an extended period of low prices in cryptocurrencies—occurred in 2018. The 2018 decline in crypto prices was partly related to large failures in initial coin offerings and concerns about imminent regulations. In contrast, the current price decline appears to be tied to macro-economic trends and rising interest rates. 4040. See DappRadar, Contrasting the 2022 Market Crash to 2018’s Crypto Winter, The Defiant (May 26, 2022), https://thedefiant.io/dappradar-winter-is-coming/ (https://perma.cc/6WYD-R2BE). It is yet to be seen whether 2022-2023 will produce another peak in litigation rates given the recent crypto meltdown.4141. The number of cases in 2018 was over 60 whereas so far in 2022, which has seen another record number of crypto-related cases, the number of cases has reached close to 30 as of October 2022.

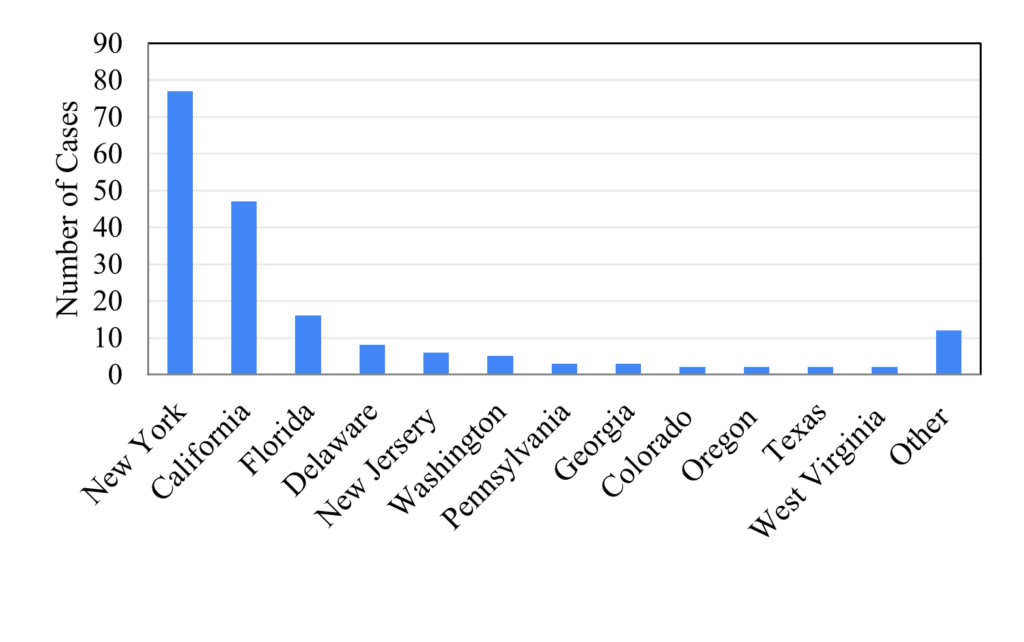

B. New York and California are the Hubs for Crypto Litigation

The data show that New York and, by a distant second, California are the go-to jurisdictions for crypto litigation. However, the concentration of claims in these jurisdictions is a relatively recent development. Earlier cases were more dispersed across jurisdictions. For instance, in 2017, 50% of all crypto-related cases were filed in New York and California courts. This percentage was close to 58% in 2018. By contrast, in 2020, more than 90% of all cases were filed in New York and California courts. Nearly 70% of all cases were filed in New York and California in the first nine months of 2022.

The data, as shown in the chart below, include both state and federal cases in each respective jurisdiction.

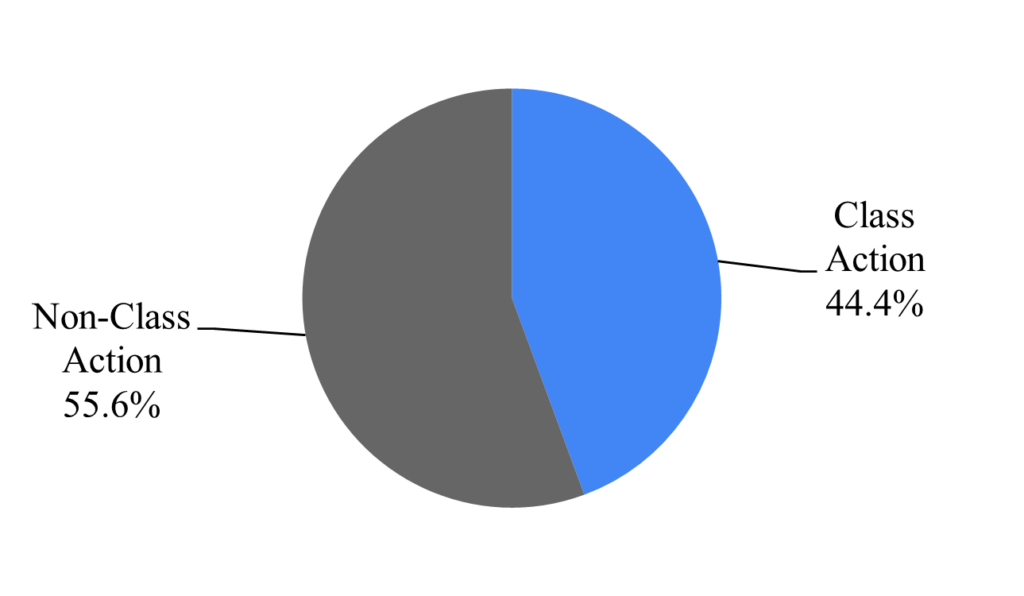

C. Class Action Lawsuits are a Major Part of Crypto Litigation

Class action cases amount to approximately 44% of all cryptocurrency cases. Most of the class action cases have arisen out of alleged violations of securities regulations and consumer protection statutes.

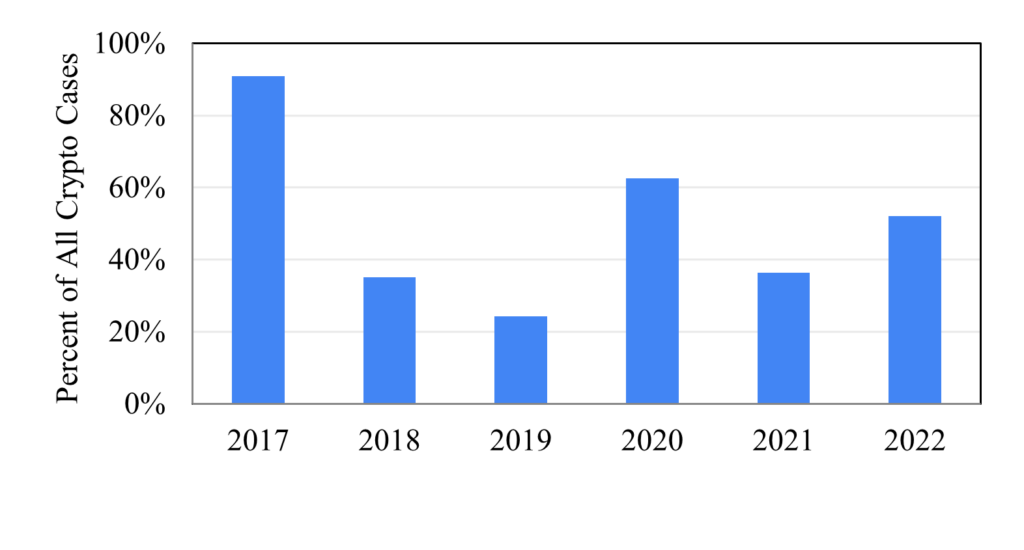

Data also show that class action lawsuits peaked in 2018. After adjusting for the percentage of total cases, the data show that class action lawsuits were the most frequent form of action early on. Note that the wave of crypto-related litigation started in 2017. Although the first cases date back to 2014, only a handful of cases occurred between 2014 and 2016. It was not until 2017 that crypto-related litigation began to gain momentum. Current rates suggest the number of class action suits may surpass the 2018 and 2020 peaks.

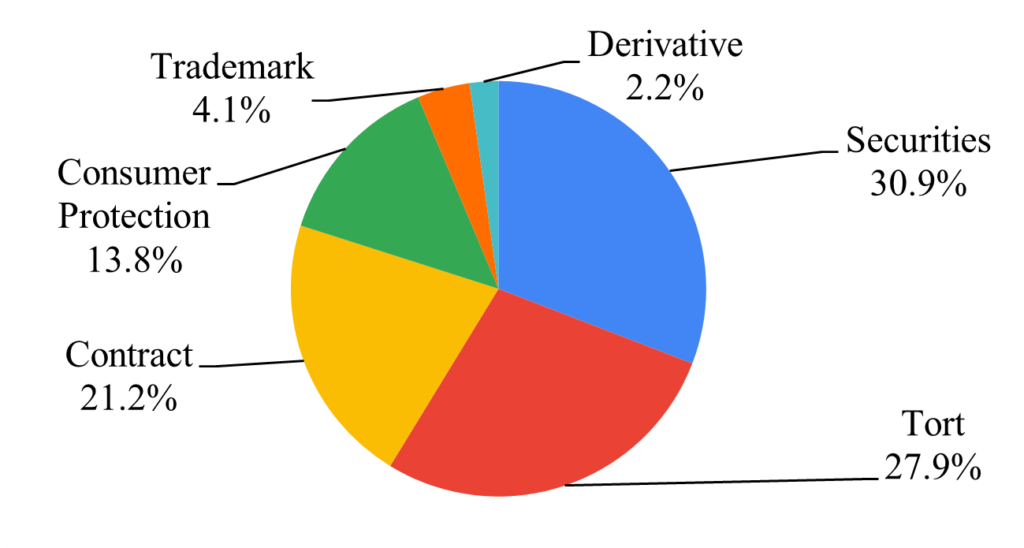

D. Securities and Tort Claims Account for Most Causes of Actions

The data show that securities allegations and tort claims have accounted for more than half of the causes of action in crypto suits, as the chart below shows. Most commonly, these cases included allegations of securities law violations arising from the sale of unregistered securities. These actions were often coupled with tort actions, such as negligent misrepresentation and fraud. Such cases arose largely due to the 2017 initial coin offering (ICO) boom and cryptocurrencies’ then-undetermined status as securities.4242. See, e.g., Nate Crosser, Initial Coin Offerings as Investment Contracts: Are Blockchain Utility Tokens Securities?, 67 U. Kan. L. Rev. 379 (2018). Examples of these cases include claims against Ripple4343. The most important securities case related to cryptocurrency is likely the one involving Ripple Labs, Inc. On December 22, 2020, the SEC sued Ripple, one of the largest cryptocurrencies by market capitalization. Complaint & Demand for Jury Trial, SEC v. Ripple Labs, Inc., No. 20-cv-10832 (S.D.N.Y. Dec. 22, 2020). In re Ripple comprises various actions alleging both violations of federal and California state securities laws. Such actions include Complaint & Demand for Jury Trial, Coffey v. Ripple Labs, Inc., No. 18-3286 (N.D. Cal. May 3, 2018); Complaint & Demand for Jury Trial, Greenwald v. Ripple Labs, Inc., No. 18-4790 (N.D. Cal. Aug. 8, 2018); Zakinov v. Ripple Labs, Inc., No. 18-CIV-2845 (Cal. Super. Ct. San Mateo Cnty. Feb 26. 2020); and Oconer v. Ripple Labs, Inc., No. 18-CIV-3332 (Cal. Super. Ct. San Mateo Cnty., June 27, 2018). and Tezos.4444. Samuel Haig, Class Action Lawsuit Targeting Tezos Ends in $25M Settlement After 3 Years, CoinTelegraph (Sept. 1, 2020), https://cointelegraph.com/news/class-action-lawsuit-targeting-tezos-ends-in-25m-settlement-after-3-years (https://perma.cc/C6SD-HDDP).

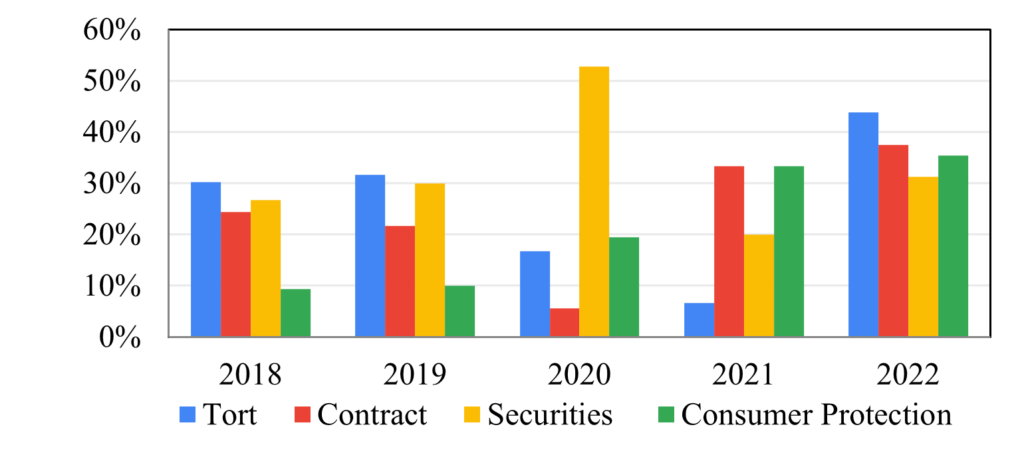

The chart below shows the breakdown of crypto cases by cause of action for each year. Though the data are incomplete for 2022, the data suggest that lawsuits under the securities laws are subsiding. By contrast, claims arising out of consumer protection laws and private law claims are on the rise. As stated above, consumer protection lawsuits include those arising out of statutes aimed to protect consumers such as California Consumer Legal Remedies Act,4545. Cal. Civ. Code § 1750 et seq. (West 2018). California Unfair Competition Law,4646. Cal. Bus. & Prof. Code § 17200 et seq. (West 2018). and Illinois Consumer Fraud and Deceptive Business Practices Act.4747. 815 Ill. Comp. Stat. § 505 (2021).

III. Crypto as Contract Litigation: Projection

What is next for crypto? The data suggest that a significant portion of crypto-related lawsuits prior to 2021 involved securities litigation. This is related to the general uncertainty regarding the status of crypto as a “security,” which notably culminated in a series of high-profile lawsuits against Ripple.4848. See Crosser, supra note 42. Tied to securities claims are tort claims based on misrepresentation. However, this is likely to change in the future.

Based on the empirical data presented, this Essay argues that the peak of securities litigation involving crypto has most likely passed. First, uncertainty over crypto assets’ status a security may be receding, given that SEC has provided more regulatory clarity.4949. Jeff Novel, Is Crypto a Currency or Security?, Reuters (Nov. 8, 2021), https://www.mondaq.com/unitedstates/fin-tech/1129220/is-crypto-a-currency-or-security-litigation-involving-the-sec-may-provide-guidance (https://perma.cc/M9TS-4LZY). Second, much of the securities litigation arose from the 2017 ICO boom.5050. Although it is possible to witness another ICO boom, given the current macro-environment and the ongoing crypto winter, it seems increasingly unlikely. Indeed, the data suggest that securities lawsuits are already giving way to cases arising from private law claims. I term this development the private law pivot.

The private law pivot refers to an increase in actions based on private tort and contract law, as well as consumer protection statutes. This shift may be the product of changes in the legal landscape, the cryptocurrency industry, and the evolution of available causes of action. Analysis of the reasons for the emergence of new causes of action requires a separate piece, but I submit that a better understanding of the inner workings and complexities of blockchain networks by attorneys and the public have contributed to this development. Overall, I project that the private law pivot stands to play an important role in regulating the cryptocurrency space.

The case Mark Shin v. ICON Foundation is illustrative of this trend.5151. em>.Shin v. ICON Foundation, No. 20-cv-07363, 2021 WL 6117508 (N.D. Cal., Dec. 27, 2021). In Shin, the enforceability of the ICON Foundation blockchain network’s “constitution” (agreement) and ownership of the awarded tokens were central to the district court’s contracts analysis. Put differently, Plaintiff Mark Shin brought a “case of first impression” arising out of contracts and property rights stemming from the enforceability of the exchange founding agreement.5252. Id. at *1. Separately, in the case of Ox Labs Inc. v. Bitpay Inc., the court sought to determine whether benefits received from Bitcoin’s “hard fork” were considered “retained” under the plaintiff’s unjust enrichment claim as a matter of law.5353. Ox Labs Inc. v. Bitpay, Inc., No. CV 18-5934, 2019 WL 6729667 (N.D. Cal. Jan. 24, 2020). Specifically, the court decided that plaintiff’s unjust enrichment claims are factual disputes as “it is unclear whether Defendant has ‘retained’ any benefits” from forks and whether “Plaintiff would be entitled to” such benefits under restitution. Id. at *8. The two “hard forks” resulted in possessors of Bitcoin receiving the same number of their Bitcoin holding in new virtual currencies called Bitcoin Cash and Bitcoin Gold. Id. at *2. On appeal, the Ninth Circuit issued an unpublished opinion in this case ruling that the claim of conversation does not extend to Bitcoin as they are “intangible.” Ox Labs Inc. v. Bitpay, Inc., 848 Fed. App’x 795, 796 (9th Cir. 2021). Another example is the recent class action brought by a putative class against a DAO for the hacking and theft of a cryptocurrency on its blockchain network based entirely on “negligence.”5454. See Complaint, Sarcuni v. bZx DAO, No. 22-cv-00618 (S.D. Cal. May 2, 2022). These cases illustrate novel issues (often internal to the inner workings of blockchain platforms) are emerging in lieu of (or in addition to) the existing largely securities fraud claims.

Based on a review of the cases to date, I have categorized cryptocurrency contract cases into (a) business-to-business breach of contract cases, (b) disagreements over sales of crypto assets, and (c) breach of fiduciary duties claims.

The first category involves breach of contract between businesses. For instance, in Polites v. Alchemy Finance, Inc., et al., the dispute concerned a one-percent commission under an advisory agreement between sophisticated parties.5555. em>.Complaint & Demand for Jury Trial, Polites v. Alchemy Finance, Inc., No. 19-cv-03862 (S.D.N.Y. Apr. 30, 2019). See also Emerging Markets Intrinsic Cayman, Ltd. v. Kadena LLC, No. 500262/2019 (N.Y. Sup. Ct. Jan. 4., 2019). A similar dispute occurred in Factset Research Systems Inc. v. CG Blockchain, Inc., which arose out of an agreement to develop an application that interfaced between parties.5656. Summons, Factset Research Systems Inc. v. CG Blockchain, Inc., No. 650027/2019 (N.Y. Sup. Ct. Jan. 3, 2019). There is little novelty arising from the nature of crypto assets in this first category; they involve business-to-business contracts in which one or both parties offer a crypto product.

The second category of cases concerns the sale of crypto assets. For example, in Hu Chun Liang v. Olympus DAO et al., a dispute arose out of the seller’s alleged failure to deliver contracted tokens. It is this second category, similar to Shin v. ICON Foundation, that implicates idiosyncratic features of crypto assets.

The third category of cases relates to the breach of fiduciary duties. The case against Tyler and Cameron Winklevoss’s crypto funds is an example in which the fund’s breach of fiduciary duties was at issue.5757. em>.Winklevoss Twins’ Fund Clears Legal Hurdle in Bitcoin Thief Case, Bloomberg Law (Jan. 8, 2019), https://news.bloomberglaw.com/securities-law/winklevoss-twins-fund-clears-legal-hurdle-in-bitcoin-thief-case (https://perma.cc/P3TA-UKSC).

This survey of the data indicates that crypto assets often create novel legal issues in contract litigation. For example, the extent to which Uniform Commercial Code warranties apply to crypto assets (and exchanges that offer crypto assets) is an increasingly important question. At the organizational level, novel issues have emerged pertaining to DAOs’ ‘form of business’ and associated liabilities.5858. Kevin S. Schwartz, et al., Wachtell Lipton Discusses Legal Considerations for Decentralized Autonomous Organizations, CLS Blue Sky Blog (June 6, 2022), https://clsbluesky.law.columbia.edu/2022/06/06/wachtell-lipton-discusses-emerging-issues-in-decentralized-governance-and-the-lessons-of-corporate-governance/ (https://perma.cc/C7SW-2FHK). DAOs also present novel ethical issues. See Ghodoosi, supra note 13. Relatedly, a host of governance issues arise from DAOs, including fiduciary duties. Another fundamental issue concerns the very notion of privity in contract law, which may not exist when organization governance is decentralized. These emerging private law issues are likely to be confronted by courts in the years to come.

Conclusion

This Essay offers the first empirical analysis of all U.S. litigation involving crypto assets. Empirical data demonstrate that crypto litigation peaked in 2018, and that class action suits alleging violations of securities laws were the main source of such historical litigation. The nature of crypto litigation, however, is changing. This Essay suggests that litigation arising from traditional private law claims and consumer protection statutes is on the rise. Based on this trend, I argue that the future of crypto litigation will involve novel issues arising out of private law: commercial warranties, decentralized enforcement, forms of business, privity, and so forth. This trend can be described as a private law pivot in crypto litigation.

The private law pivot comes amid an increase in decentralized platforms with distributed governance structures offering crypto assets. This new pivot, like the ICO trend of 2018, is likely to create a host of complex challenges arising out of the novelty of these claims, the complexity of blockchain networks and the crypto-asset ecosystem, and the enforcement of judgments in decentralized networks in which users are anonymous. These challenges, however, can pave the way for emerging private legal ordering of the crypto-asset ecosystem which can in turn support wider adoption of crypto assets. In short, my prediction is that the private law pivot will lead to a more developed private legal ordering with clearer precedents on issues such as enforceability, warranties, fiduciaries duties, and business torts, ultimately leading to more public awareness, and possibly trust, in crypto assets.

†Assistant Professor of Business Law, California State University, Northridge, David Nazarian College of Business & Economics, Department of Business Law. Project Lead, Autonomy in Law at NASA-Launched Autonomy Research Center for STEAHM (ARCS); Former Ripple-Fintech faculty fellow; JSD, LLM (Yale Law School), LLM in Business Law (U.C. Berkeley Law School.) I would like to thank The Autonomy Research Center for STEAHM for their support of this project and Toan Pham and Icess Iana Nisce for helpful assistance.

Replication data for this paper is available on JREG’s Dataverse account.