Was the SPAC Crash Predictable?

PDF DownloadIn this Essay, we revisit our analysis in A Sober Look at SPACs and assess whether that analysis—based on the 47 SPACs that merged between January 2019 and June 2020—provided a basis on which to predict that the dilution embedded in the SPAC structure would lead to severe shareholder losses in subsequent mergers. We find that our prior analysis has been borne out in the 243 SPACs that merged in the 18 months that following the period of our original analysis. Consistent with our original analysis, after accounting for the value that sponsors, bankers, and IPO investors extracted from SPACs, there was little net cash underlying SPAC shares as SPACs entered into mergers in this recent period. In addition, the amount of net cash underlying those shares continued to be highly correlated with post-merger share value, as in our original analysis. For this analysis of more recent mergers, we take advantage of the much larger number of SPAC mergers to control for the influence of potentially confounding factors in the relationship between pre-merger net cash per share and post-merger share value. In short, we find that the SPAC crash of 2021 and 2022 was predictable.

Special purpose acquisition companies, or “SPACs,” have delivered poor post-merger returns to shareholders for many years.11.Michael Klausner, Michael Ohlrogge & Emily Ruan, A Sober Look at SPACs, 39 YALE J. ON REGUL. 228, 259-60 (2022) [hereinafter Sober Look]. In A Sober Look at SPACs, first released in October 2020, we analyzed the 47 SPACs that merged between January 2019 and June 2020 and reached two central conclusions that we believe explain SPACs’ poor performance.22.Id. First, the SPAC structure is highly dilutive. We found that, at the time of a SPAC’s merger, SPACs held far less than $10 in net cash per share, which is both the approximate price at which shareholders may redeem their shares and, typically, the value that SPACs attribute to their shares when they merge. Second, we found a strong correlation between a SPAC’s pre-merger net cash per share and its post-merger market-adjusted returns, which, on average, were roughly negative 50% as of 18 months following a merger. Although we recognized that correlation does not necessarily imply causation, we explained that there is a clear logical connection between pre-merger net cash per share and post-merger share price, and we therefore viewed the correlation as indicative of a causal relationship. Hence, the dilution inherent in the SPAC structure appeared to explain SPACs’ poor past performance and to portend poor performance in the future.

Notwithstanding SPACs’ poor performance (and our analysis showing that their poor performance was a consequence of their structure), the number of SPAC IPOs and SPAC mergers skyrocketed in 2020 and 2021. In the middle of that time period—Q4 of 2020 and Q1 of 2021—SPAC mania grew to a point at which SPACs were trading well above their cash value before they announced mergers and higher still upon their announcement of a deal and thereafter.

By the beginning of 2022, however, the SPAC crash had begun. Post-merger returns for the SPACs that merged over the prior year and a half had fallen dramatically, even compared to market indices and traditional IPOs. As of December 1, 2022, SPACs that merged between July 2020 and December 2021 had an average share price of $3.85, down over 60% from the $10 per share that SPAC shareholders could have received if they redeemed their shares.33.Comparing these returns to benchmark indices, the average post-merger SPAC underperformed against the Nasdaq by 44% and underperformed against the Russell 2000 by 51%. The average post-merger SPAC during this period underperformed the average traditional IPO by 26%. Fitting one, three, and five factor models for each SPAC’s daily post-merger prices and taking the average alpha across all SPACs, yields annual underperformance of 52%, 37%, and 31% for the one, three, and five factor models, respectively. Thus, by all indicators, SPACs’ recent performance has continued to be quite poor, even in the turbulent conditions that have beset markets in general. Moreover, for the six months prior to December 1, there were only 16 new SPAC IPOs, a 93% decline from the same period in 2021. News reports in 2022 confirmed that SPACs had lost their luster and were no longer viewed as the miraculous financial innovation that some had imagined.44.See, e.g. Yun Li, SPAC Market Hits a Wall as Issuance Dries Up and Valuation Bubble Bursts, CNBC (Aug. 3, 2022), https://www.cnbc.com/2022/08/03/spac-market-hits-a-wall-as-issuance-dries-up-and-valuation-bubble-bursts.html (https://perma.cc/C5YQ-4WGJ); see also Tom Zanki, The SPAC Crash Forces Merger Targets To Rethink Strategies, Law 360 (July 22, 2022), https://www.law360.com/articles/1514217/the-spac-crash-forces-merger-targets-to-rethink-strategies (https://perma.cc/K3FV-3R6J).

The analysis in Sober Look supported a prediction that SPACs would crash. But it was based on just 47 SPAC mergers that closed over an 18-month period. Perhaps the dilutive structure of SPACs would change, or perhaps the relationship between pre-merger dilution and post-merger value would not persist. In this brief follow-up Essay, we look back and ask whether either of these breaks with the past occurred. In addition, with the larger number of SPACs that merged between mid-2020 and the end of 2021, we look more deeply into our inference that low net cash per share caused SPACs’ poor post-merger performance. In effect, using more data and more recent data, we revisit the prediction in Sober Look that the SPAC crash would happen. Our results are consistent with our results in Sober Look, and our conclusion is that the SPAC crash was predictable. We further predict, therefore, that to the extent that SPACs persist after the crash, they will continue to deliver poor returns to non-redeeming investors unless their structure is substantially reformed.55.Furthermore, as we explain in in another paper, some changes in the SPAC structure that are widely celebrated as reforms and improvements are neither new nor particularly useful in resolving SPACs’ core challenges. See Michael Klausner & Michael Ohlrogge, Is SPAC Sponsor Compensation Evolving? A Sober Look at Earnouts (Stanford L. and Econ. Olin Working Paper No. 567) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4022611 (https://perma.cc/4739-9TE9). The continued importance of cash per share that this paper documents supports the decision of the Delaware Court of Chancery that net cash per share is material information that must be disclosed to SPAC shareholders when they choose whether to redeem their shares or invest in a proposed merger.66.Richard Delman v. GigAquisitions3, LLC, C.A. No. 2021-0679-LWW (Del. Ch. Jan. 4, 2023) Our findings also reinforce the need for the SEC to require disclosure of net cash underlying SPAC shares.77.Michael Klausner, Michael Ohlrogge & Harald Halbhuber, Net Cash Per Share: The Key to Disclosing SPAC Dilution, 40 Yale J. on Regul. Bulletin 18 (2022).

I. Prior Efforts to Explain Poor SPAC Performance

A Sober Look at SPACs was the first economic investigation to focus on current generation SPACs, which emerged in 2009.88.There have been three generations of SPACs, with the most substantial structural change occurring in the third, current generation. For a discussion of the transition from second generation to third generation SPACs, see Usha Rodrigues & Mike Stegemoller, Exit, Voice, and Reputation: The Evolution of SPACs, 37 Del. J. Corp. L. 849 (2012). Shortly after Sober Look, Minmo Gahng, Jay Ritter and Donghang Zhang posted an article that reached similar results as Sober Look regarding returns to SPAC shareholders, while adding additional analyses on post-merger returns to SPAC warrant holders.99.Minmo Gahng, Jay R. Ritter & Donghang Zhang, SPACs, Rev. Fin. Stud. (forthcoming 2023). The article by Gahng et al. did not develop new theories for why historical SPAC performance was poor,1010. Gahng et al. briefly discussed the theories advanced in Sober Look to explain poor SPAC performance, but it did not take a stand endorsing or rejecting those theories. Gahng et al. also suggest that poor post-merger performance may be due to SPACs taking “low-quality” companies public, due in part to bad sponsor incentives. Id. As we explain in this section, “low-quality” companies and sponsor incentives cannot explain why SPACs regularly fail to find deals that perform well for post-merger investors. but did express optimism that the market was in the midst of moving to a sustainable equilibrium in which post-merger SPAC returns would improve. We saw no basis for such optimism at the time Sober Look was published, and we confirm here that the optimism was not well founded.

Several years prior to Sober Look, there was a literature on pre-financial crisis SPACs,1111. See, e.g., Ioannis V. Floros & Travis R.A. Sapp, Shell Games: On The Value of Shell Companies, J. Corp. Fin. 850 (2011); Milan Lakicevic & Milos Vulanovic, A Story on SPACs, 39 Managerial Fin. 384 (2013); Usha Rodrigues & Mike Stegemoller, What All-Cash Companies Tell Us About IPOs and Acquisitions, 29 J. Corp. Fin. 111 (2014). but the structure of those SPACs differed from that of current SPACs in important ways. Like current SPACs, however, pre-2009 SPACs were highly dilutive, yet none of the literature at the time viewed dilution as a critical factor in explaining SPACs’ poor post-merger performance.1212. See, e.g., Sris Chatterjee, N. K. Chidambaran & Gautam Goswami, Security Design For a Non-Standard IPO: The Case of SPACs, 69 J. Int’l. Money & Fin. 151, 157 (2016) (arguing that dilution from warrants granted to SPAC investors, but not sponsors, actually improves SPAC governance by reducing sponsor incentives for risk-taking); David Miller, SPAC IPOs in 2008, Financier Worldwide (2008) (describing dilution from SPAC warrants as a potential problem for target companies, not for SPAC shareholders); Lakicevic & Vulanovic, supra note 11, at 392-93 (discussing dilution of ownership interests due to the sponsor’s promote as a feature of SPACs, but not linking this feature to post-merger performance); Milos Vulanovic, SPACs: Post-Merger Survival, 43 Managerial Fin. 679, 686-90 (2017) (discussing dilution as a feature of SPACs and one that is potentially relevant to whether post-merger firms stay listed on exchanges, but not discussing its relationship to post-merger share prices). The papers that came closest to our analysis of the impact of dilution are Stefan Lewellen, SPACs As An Asset Class, at 11-12 (Mar. 24, 2009) (unpublished manuscript), https://ssrn.com/abstract=1284999 (https://perma.cc/D3GN-86Y4) (noting that when warrants are exercised post-merger they may lower share prices, but not analyzing whether SPAC or target shareholders bear the cost of the warrant overhang, nor analyzing other sources of dilution or dissipation of cash, nor positing that such dilution could play a major explanatory factor in SPAC returns) and Tim Jenkinson & Miguel Sousa, Why SPAC Investors Should Listen To The Market, 21 J. Applied Fin. 38, 41-42 (2011) (noting that whether pre-merger SPAC shares trade above redemption prices reflects whether the market views the sponsor to have added enough value to account for the 20% promote it receives, but not examining any relationship between the promote and post-merger returns). Johannes Kolb and Tereza Tykvová speculated that poor post-merger performance was due to SPACs taking “lower-quality” firms public,1313. Johannes Kolb & Tereza Tykvova, Going Public Via Special Purpose Acquisition Companies: Frogs Do Not Turn into Princes, 40 J. Corp. Fin. 80, 91, 93 (2016). and Vinay Datar, Ekaterina Emm, and Ufuk Ince offered a similar explanation.1414. Vinay Datar, Ekaterina Emm & Ufuk Ince, Going Public Through The Back Door: A Comparative Analysis of SPACs and IPOs, 4 Banking & Fin. Rev. 17, 31-33 (2012). Yet even if a target is low-quality in some respects, a merger could still be value-enhancing for SPAC shareholders if the SPAC acquires a stake in that target for an advantageous price. These studies focusing on target quality did not attempt to explain why SPACs would systematically overpay when negotiating mergers.1515. A company with any value can be a good investment at the right price and a bad investment at the wrong price. Thus, the notion that SPACs perform poorly because they merge with “low-quality” companies makes little sense; it is the pricing of companies that matters for SPAC returns, not the “quality.”

Two articles offered explanations for earlier SPACs’ poor post-merger performance based on incentives. Lora Dimitrova argued that bad incentives for SPAC sponsors were a key driver of poor performance,1616. Lora Dimitrova, Perverse Incentives Of Special Purpose Acquisition Companies, The “Poor Man’s Private Equity Funds” 63 J. Acct. & Econ. 99, 118 (2017) (examining the deadlines that SPAC charters provided to complete a merger or liquidate, and finding that SPACs that merged closer to these deadlines did worse, potentially indicating that sponsors of these SPACs had particularly bad incentives to propose a bad merger rather than allow a liquidation). and John Howe and Scott O’Brien found that directors with ties to SPAC sponsors have incentives to approve mergers that sponsors support but that will be bad for SPAC shareholders.1717. John S. Howe & Scott W. O’Brien, SPAC Performance, Ownership and Corporate Governance, 15 Advances Fin. Econ. 1 (2012). We agree that sponsors’ incentives and a lack of director independence are problematic.1818. See Richard Delman v. GigAquisitions3, LLC, C.A. No. 2021-0679-LWW, at 4 (Del. Ch. Jan. 4, 2023); In re MultiPlan Stockholders Litigation, Consolidated C.A. No. 2021-0300—LWW, at 3 (Del. Ch. Ct. Jan. 3, 2022); Sober Look, supra note 1, at 247; Michael Klausner & Michael Ohlrogge, SPAC Governance: In Need of Judicial Review 6-9 (NYU L. & Econ. Research Paper No. 22-07, Stan. L. & Econ. Olin Working Paper No. 564 (2022)), https://ssrn.com/abstract=3967693 (https://perma.cc/3BLC-5GF5) (noting that what is problematic about sponsor incentives is that a sponsor will prefer a bad deal over no deal, not that sponsors will not try hard to find the best deal that they can). But these are not explanations for why SPACs systematically fail to negotiate mergers that are value-enhancing for shareholders and sponsors alike. Sponsors do not lack incentives to strike deals that are good for shareholders. They systematically fail to do so, however. What is needed is an explanation for why that is. As we explained in Sober Look and as we confirm below, the answer lies in the dilution and dissipation of cash inherent in the SPAC structure, and the resultant deal a SPAC can expect in a merger with a target.

II. Pre-Merger Net Cash Per Share and Post-Merger Share Value

Our analysis in Sober Look explained the historically poor performance of SPACs by exposing the extent to which SPACs’ equity is highly diluted at the time they merge, and by showing a high correlation between pre-merger dilution and post-merger performance. We further showed that SPACs offer few transactional or legal advantages that compensate for their cash shortfalls. Based on that analysis, one would predict that if the structure of SPACs remained unchanged, future SPAC performance would be poor. In the analysis below, we analyze the extent to which a more recent cohort of SPACs are diluted and the extent to which that dilution is related to post-merger performance.

A. Dilution and Dissipation of Cash

In a SPAC’s IPO, the SPAC typically sells units consisting of one share and a warrant for a fraction of a share for $10. When a SPAC’s board presents shareholders with a proposed merger, shareholders have a right to redeem their shares for $10 plus accrued interest or to hold onto their shares and invest in the proposed merger. The IPO investors thus get the warrants as an inducement to buy units in the IPO. When a SPAC merges with a target, it typically does so in a share exchange. The post-merger combined company will hold the cash that the SPAC contributes and the business of the target; and the shareholders of the SPAC and the target will become shareholders of the combined company.

SPACs typically value their shares at $10 in their share exchange with a target.1919. SPACs do this because, prior to a merger, a share provides a right to redeem at approximately $10 per share, which puts a floor on the trading price of a pre-merger SPAC share. Apparently, SPAC boards feel that they need to adopt the $10 share price as a basis for their stock-for-stock exchange despite the fact that the actual value of a share has no connection to that price. SPACs vary in their proxy statements with respect whether they explicitly claim that their shares are actually worth $10. But a SPAC’s only asset, and hence, the only asset the SPAC will contribute to a merger, is cash. While a SPAC’s IPO investors pay $10 per unit, that $10 begins to be diluted immediately. In Sober Look, we found that the mean and median amount of net cash per share in SPACs that merged from January 2019 through June 2020 was $4.10 and $5.70, respectively.2020. We use the term net cash per share to refer to cash per share net of the implicit cost of the warrant overhang, which, consistent with SEC guidance, we treat as a liability. So, about half of the supposed $10 value of a SPAC share had vanished before the SPAC even completed its merger. The lost value is attributable to dilution caused by (a) warrants that SPACs include in the units they issue in their IPO, (b) in some cases, rights to 1/10 or 1/20 of a share for free that that SPACs include in their units, (c) additional warrants that SPACs issued to their sponsor, (d) compensation SPACs pay to their sponsor in the form of 20% of post-IPO equity, and (e) in some cases, convertible debt or additional warrants. In addition, SPACs lose additional cash as a result of deferred fees paid to IPO underwriters at the time of a merger and substantial additional payments to financial advisors in connection with mergers.2121. For a breakdown of these costs, see Sober Look, supra note 1, at 252.

At the time of a SPAC’s merger, there are also two sets of transactions working in opposite directions that can either exacerbate or ameliorate the loss of net cash per share. Public shareholders have a right to redeem their shares rather than invest in a proposed merger. To the extent they do, net cash per share drops. Although redemptions reduce both cash and shares, the proportionate reduction in cash (the numerator) is higher than the proportionate reduction in shares (the denominator).2222. In the numerator, the cost of outstanding warrants and the fees paid to bankers are typically not reduced in response to redemptions. In the denominator, sponsor shares remain unchanged. At the same time, in conjunction with the merger, a SPAC often brings in new equity through private investment in public equity, or “PIPEs.” This investment has the opposite effect of redemptions on net cash per share, increasing the cash in the SPAC without a proportionate increase in costs. The net effect of redemptions and PIPEs depends on the volume of each and the price PIPE investors pay for shares.

B. The Connection Between Pre-Merger Net Cash Per Share and Post-Merger Share Value

There are two links between a SPAC’s pre-merger net cash per share and the value of SPAC shareholders’ post-merger holdings. First, the more cash a SPAC contributes to the combined company, the more valuable shares in the combined company will be, all other factors held constant. And, since the SPAC’s warrants become warrants of the combined company, the more warrants the SPAC has outstanding, the greater the dilutive overhang on post-merger shares, and hence the lower the value of those shares.2323. As we explain below, although warrants will overhang the value of all post-merger shares, this does not mean that all post-merger shareholders will bear the costs of those warrants equally. Target company owners can fully immunize themselves from the dilutive effect of warrants by structuring the merger so that the number of shares they receive in the merger, times the value of those shares (after accounting for warrant overhang), equals the value of the per-merger company. Net cash per share, which measures cash underlying a SPAC share net of the value of outstanding warrants, is thus directly related to the value of post-merger shares.2424. For a detailed analysis of why net cash per share is the correct measure of a SPAC share’s value, and an explanation of how to calculate it, see Michael Klausner, Michael Ohlrogge & Harald Halbhuber, Net Cash Per Share: The Key to Disclosing SPAC Dilution, 40 Yale J. on Regul. Bulletin 18 (2022).

The second link between pre-merger net cash per share and post-merger share value lies in the fraction of the target that SPAC shareholders can expect to receive in a share-for-share exchange. The value SPAC shareholders receive will depend on how many shares the SPAC issues to target shareholders, which in turn depends on the value of the SPAC’s shares. The more shares issued to the target, the lower the SPAC shareholders’ interest in the post-merger company will be. As stated above, SPACs have followed a practice of valuing their shares at $10 in share-for-share mergers with targets—roughly their redemption price. SPACs therefore issue to target shareholders a number of shares equal to the agreed-upon value of the target divided by $10. If, however, a SPAC will deliver, say, $5 in net cash per share to the target, the SPAC’s $10 per share valuation is twice its actual value, and the SPAC will underpay target shareholders by half. A reasonable expectation, therefore, is that target shareholders—who are often venture capital funds, private equity funds or other sophisticated investors—will respond by attempting to negotiate a valuation for the target that is twice the target’s actual value, in which case the SPAC will issue twice as many shares to the target’s shareholders.2525. For more detail on how targets can structure SPAC merger agreements to pass SPAC dilution costs on to SPAC shareholders, see Sober Look, supra note 1, at note 40 and accompanying text. If the target shareholders succeed, the result will be that they receive shares worth the value of their pre-merger ownership stake in the target, and SPAC shareholders will be left with shares worth $5. That is, in exchange for each SPAC share worth $5 in net cash, the target will exchange $5 worth of value, and SPAC shareholders will see their share value drop from a redemption price of $10 to a post-merger price of $5.2626. For simplicity, we have assumed in this example there is no surplus created in the transaction, or alternatively, that any enhancement of the target’s value created by the transaction will be captured by the target owners, which is what one would expect in efficient, competitive capital markets. See for instance, Christopher B. Barry, Initial Public Offering Underpricing: The Issuer’s View—A Comment, 44 J. Fin 1099, 1101 (1989) (arguing that when owners of a private firm take it public, if those owners receive anything less than the full value of the newly public corporation, minus the new cash contributed to it, then it represents a “cost” of the going public transaction).

It is possible that a merger between a SPAC and a target creates surplus value—that a target sees value in combining with a SPAC beyond the net cash it will receive—in which case the target may agree to a deal that does not inflate its value commensurately with the inflation of the SPAC’s valuation of $10 per share. In that case, the merger may be profitable for both target and SPAC shareholders. Perhaps a SPAC’s sponsor has skills or experience that it will use to add value to the post-merger company, or perhaps value is created simply by going public. In Sober Look, we found that the market on average anticipated some surplus at the time of a merger, but that this expectation dissipated as the market observed post-merger performance over time, and post-merger share prices declined.2727. Sober Look, supra note 1, at 261. Similarly, we found that the transactional and legal advantages attributed to SPACs, which could potentially be a source of deal surplus, ranged from completely spurious to greatly overstated.2828. Id, at 274-78. We do not, however, deny the possibility of surplus value in individual cases.

If a merger does not generate enough surplus to enable both target and SPAC shareholders to come out ahead, then one might expect SPACs to resist target efforts to negotiate a deal in which they receive post-merger shares roughly equal in value to the net cash the SPAC delivers. A SPAC’s management and sponsor would prefer a better deal to a worse deal, but they would also prefer a deal that is bad for SPAC shareholders over a liquidation in which they would gain nothing and the sponsor would lose its initial investment in the SPAC.2929. Sober Look, supra note 1, at 247. Therefore, if target shareholders are only willing to enter into mergers that overstate target values to match overstated SPAC values, we would expect SPAC sponsors and management to acquiesce to target overvaluation rather than face liquidation. It is also not surprising that unsophisticated shareholders go along with these deals to a large extent, especially in light of the hype that accompanied SPACs over the past few years.

The parties one would most expect to resist a bad deal are PIPE investors, who in general are sophisticated. But there are reasons to believe that PIPE investors’ resistance may be less strenuous than one might expect. First, they do not always pay $10 per share. In Sober Look, we found that PIPE investors often paid a discounted price or received side payments from sponsors,3030. em>.Id. at 239. which at least in some cases are not disclosed.3131. In comments to the Wall Street Journal, Michael Klein, the sponsor for Churchill III, stated that he had given away (to parties including his PIPE investors) all promote shares in Churchill III that were not subject to vesting requirements. Churchill III’s proxy specified that 55% of promote shares were not subject to vesting requirements, meaning Klein’s claimed share transfers were for 55% of his promote. Yet, the proxy itself discloses a far smaller number of transfers of promote shares. Thus, it appears that Klein admitted in his comments to the Wall Street Journal that he had made undisclosed transfers of promote shares to PIPE investors. See Amrith Ramkumar, SPAC Insiders Can Make Millions Even When the Company They Take Public Struggles, Wall St. J., Apr. 25, 2021, https://www.wsj.com/articles/spac-insiders-can-make-millions-even-when-the-company-they-take-public-struggles-11619343000 (https://perma.cc/D22Y-BRH9). In confidential conversations, we have been told of other instances of undisclosed side payments being made. Second, because post-merger share prices are often above $10 for periods of time,3232. For instance, in Sober Look, supra note 1, at 260 fig.9, we show that returns one week after a SPAC’s merger with a target are consistently in line with those of benchmark indices. PIPE investors may adopt profitable hedging and trading strategies under which they come out ahead.3333. Indeed, while some PIPE agreements explicitly prohibit PIPE investors from shorting SPAC shares pre-merger, others do not even contain this prohibition. For an example of an agreement prohibiting pre-merger shorting, see Experience Inv. Corp., Form 424(B)(3) (Apr. 6, 2021). For examples that do not contain this, see Northern Star Acquisition Corp., Form 8-K (Dec. 17, 2020); see also Newborn Acquisition Corp., Form 8-K (Mar. 25, 2021). Third, some PIPE investors are index funds or funds specializing in particular industries such as electrical vehicles, and may invest in post-merger SPACs to mirror segments of a market. Finally, some individuals working for institutional investors may get caught up in the hype themselves.

Ultimately, the connection between pre-merger net cash per share and post-merger value boils down to a simple intuition: if a SPAC enters a negotiation with less to deliver for each of its outstanding shares, it is likely to achieve a worse outcome for its shareholders. Assuming target shareholders do sufficient due diligence, they can discover a SPAC’s net cash per share with reasonable accuracy as of the time of their negotiation with the SPAC.

Nevertheless, the extent to which targets negotiate deals in which they receive net cash equal to the value of the shares they give up is an empirical question. We investigated this in Sober Look, and we extend that investigation here. A challenge in this investigation is that, even if one observes a strong relationship between pre-merger net cash per share and post-merger value, there are two factors that might confound a causal inference.

First, as we recognized in Sober Look,3434. Sober Look, supra note 1, at 262 n.58. the market’s evaluation of a proposed merger influences redemptions, which in turn directly reduce net cash per share.3535. Redemptions reduce both SPAC cash and SPAC pre-merger shares, but the proportional redemption in cash is greater than the proportional redemption in shares. The market’s evaluation of a merger also influences post-merger share value. So, while there is a logical connection between pre-merger net cash per share and post-merger share price, the empirical measurement of that relationship may be complicated by the fact that the market’s evaluation of a deal can separately affect both pre-merger cash per share and post-merger share price. To the extent that a target can anticipate the market response and redemptions in a deal it negotiates, redemptions will not confound our inference regarding the role of cash per share. In this situation, targets can decide whether a deal, given expected redemptions, will deliver enough cash per share to compensate for the ownership interests SPAC shareholders will receive.3636. It would be astonishing if sophisticated target owners were to sign a SPAC merger agreement while giving no consideration to what potential redemptions may be, or if they naively assumed that redemptions would certainly be zero. Available evidence suggests this is not the case. In the twelve months from August 1, 2021 through August 1, 2022, 46 SPAC mergers were terminated, frequently by the election of the target company. This surge in SPAC deal cancellations coincides with a surge in redemptions for mergers that do close (70% average redemptions in the past twelve months, compared to 28% in the twelve months prior), and thus a surge in expectations for redemptions of deals set to close in the future. The proposed merger of Kin Insurance with Omnichannel Acquisition Corp. is instructive of this point. According to press accounts, in January 2022 Kin canceled the merger agreement that it had signed with Omnichannel in favor of a round of private financing that offered it a lower valuation than the SPAC merger agreement had. Lucinda Shen & Kia Kokalitcheva, Kin Insurance Gets New Funding After Spurning its SPAC, Axios, Jan 28, 2022, https://www.axios.com/2022/01/28/kin-insurance-spac-omnichannel-stock (https://perma.cc/K6BB-CSRD). If targets only cared about the valuation assigned to them in a merger agreement, and gave no thought to whether that value was sufficiently “generous” to make up for SPAC’s low cash per share, this occurrence would be difficult to explain. But, where information becomes available after the merger agreement is signed and before the redemption deadline, that information can influence both cash per share (through the redemption channel) and post-merger share price. In that scenario, our inference of the causal relationship between pre-merger net cash per share and post-merger share price will be confounded.

Second, as we also recognized in Sober Look,3737. Sober Look, supra note 1, at 253. SPACs with more skilled or experienced sponsors may tend to have higher net cash per share, but they may also achieve better deals for SPAC shareholders for reasons unrelated to the cash per share they deliver. Experienced sponsors with reputations in the market may attract more PIPE investments, conduct IPOs with warrants for a smaller fraction of a share, and convince investors not to redeem their shares. If so, the result is more net cash per share. These same sponsors, however, may also be able to achieve better outcomes for shareholders for independent reasons by negotiating better deals for SPAC shareholders, or by remaining involved with post-merger companies and creating value (which could be one reason why they can negotiate better deals). Consequently, we may not be able to fully isolate the impact of net cash per share on post-merger share value.

In our empirical analysis below, we work to address these two concerns that could confound empirical confirmation of the relationship between net cash per share and post-merger share price.

C. Analysis

In Sober Look, we analyzed SPAC mergers that occurred between January 2019 and June 2020 and found that pre-merger net cash per share was highly correlated with post-merger share price. In fact, the regression showed a nearly one-to-one relationship between pre-merger net cash per share and market-adjusted post-merger share price—that is, on average, a dollar less in net cash per share meant a dollar less in post-merger value for SPAC shareholders.3838. We found that the slope relating pre-merger cash per share to post-merger share value was similar regardless of whether we examined prices measured as of one-week post-merger, one-year post-merger, or prices as of November 1, 2021, the latest date data was available for the paper. The main differences between these time frames were first, as more time elapsed post-merger, the intercept shrunk, and second, as more time elapsed post-merger, the R2 increased. See Sober Look, supra note 1, at 261. So, during that time period, SPAC shareholders appeared to bear the full marginal cost of SPACs’ dilution. Our results also suggested that the market did not ultimately conclude that a SPAC merger created much surplus in value—that is, it did not place significant value on the post-merger contributions of former SPAC sponsors or managers remaining involved with the company.

We separated SPACs into those we defined as “high quality” and others. High-quality SPACs were defined as those whose sponsors were affiliated with private equity or venture capital funds with over $1 billion in assets under management, and those whose sponsors were led by former top executives of Fortune 500 companies (acknowledging that this was only a rough measure of sponsor quality). We found that high-quality SPACs both had more pre-merger net cash per share than the others, and that their post-merger value was higher on average. As was true of the full set of 47 SPACs, however, high-quality SPACs were still losing propositions for their shareholders, and also showed a nearly one-to-one relationship between pre-merger net cash per share and post-merger share value.

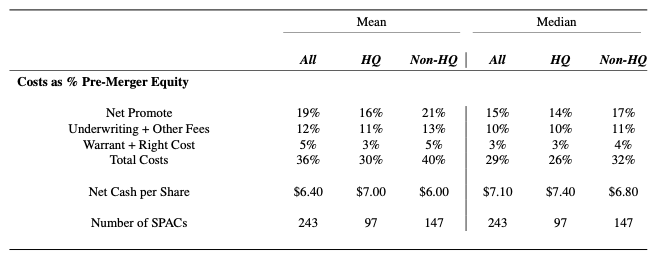

We now perform the same analysis, and some new extensions, using newly collected data on the 243 SPACs that merged between July 2020 and December 2021—the year and a half following the sample analyzed in Sober Look. We start with Table 1, which measures SPAC costs and pre-merger net cash per share.3939. For a detailed discussion of how we compute SPAC cash per share, see Sober Look, supra note 1, 252 n.37. See also Klausner et. al, supra note 24. Compared to SPACs in the Sober Look time period, SPAC costs have become somewhat lower and thus cash per share somewhat higher, but on average, SPAC costs still drained 36% of pre-merger equity and thus delivered only $6.40 in net cash for each share they exchanged with target shareholders. Much of this improvement in net cash per share is driven by the SPAC bubble that ran roughly from Q4 of 2020 through Q1 of 2021. Pre-merger SPAC prices soared during this period, which resulted in very low redemptions and much larger PIPEs. As a result, net cash per share during the bubble period was higher than it had been before or would be later. If we exclude deals that were announced or completed during this six-month window, mean and median cash per share drop by about $1.00 per share to $5.50 and $6.00, respectively. Lastly, in Table 1, we see that high quality (“HQ”) sponsors have lower costs, but this difference is much more modest than the average $5.30 difference in mean net cash per share between high-quality SPACs and other SPACs that we documented in Sober Look. Most of the change is attributable to non-high-quality sponsors attaining meaningfully higher net cash per share than they did in the Sober Look sample period.

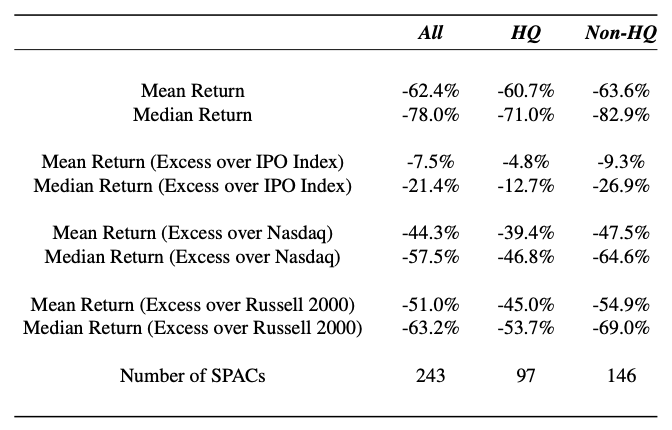

In Table 2 we examine post-merger returns, measured up to December 1, 2022. As with the January 2019 through June 2020 mergers examined in Sober Look, overall post-merger returns remain quite poor in the year and a half since then. Average post-merger returns are negative 62%; returns in excess of the Nasdaq are negative 44%; and returns in excess of the Russell 2000 are negative 51%. When adjusted by the Renaissance Capital IPO index, average returns are negative 8%, which is better than their negative 50% adjusted return in the Sober Look time period. Nevertheless, SPAC performance against IPOs may be worse than the IPO index adjusted returns suggest. The IPO index tracks performance of IPOs over a rolling two-year window following their offering date. As a result, the returns on the IPO index reflect a large number of traditional IPOs that were conducted before our sample period began. If we look at the performance of all traditional IPOs from July 2020 through December 2021, we find average returns of negative 36%,4040. For these calculations, we obtain a list of all 480 traditional IPOs that were conducted during this period from IPOscoop.com. We compute returns based on the offering price. If we compute returns based on the price after the close of the first day’s trading, that is, using the so-called “post-IPO-pop price,” we get average returns of negative 48% for traditional IPOs. This is still 14 percentage points better than the returns to SPAC mergers during this period. Furthermore, given the extensive documentation of poor returns earned by investors who buy in at the post-IPO-pop price, the fact that SPACs underperform less against this benchmark is hardly a ringing endorsement of their returns. See Jay R. Ritter & Ivo Welch, A Review of IPO Activity, Pricing, and Allocations, 57 J. Fin. 1795, 1818 (2002). which means the average SPAC merger underperformed the average IPO by 26 percentage points4141. In Sober Look, we also consider SPAC returns weighted by the amount of money left in SPAC trusts after redemptions. If SPAC investors are successful at distinguishing good deals from bad, these returns may be better than simple average returns. For the period from July 2020 and December 2021, average SPAC merger returns, weighted by post-redemption cash in trust, are negative 54%. Thus, even with this metric, SPAC mergers underperformed traditional IPOs by 18 percentage points. during our sample period.4242. The sample period we study includes both large rises and sharp drops in broad equity markets such as the Nasdaq and the Russell 2000. If SPAC mergers were more likely to occur during peaks in the equity markets, and thus more susceptible to subsequent drops, then this might explain their worse performance compared to traditional IPOs, yet not imply that their expected returns to investors are fundamentally worse. To examine this, we investigate the returns of traditional IPOs in excess of the Nasdaq and Russell 2000 benchmark indices, just as we do with SPACs. If SPACs’ worse performance were simply attributable to worse market timing, then they should perform relatively better when using returns in excess of market indices. Yet, the average returns to traditional IPOs in excess of the Nasdaq and Russell 2000 are both negative 31%, which is notably better than the negative 44% and negative 51% returns of SPACs in excess of those indices.

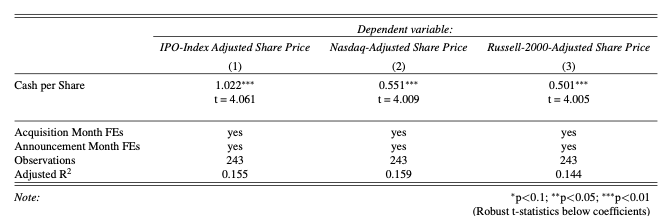

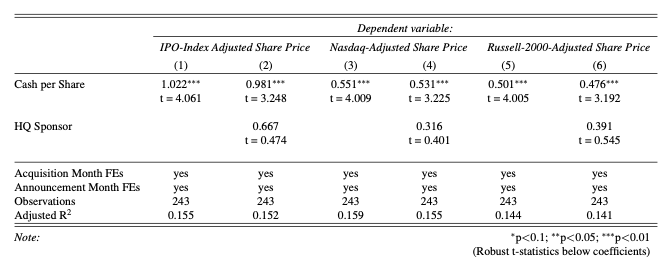

On the whole, the costs embedded in SPACs that merged between July 2020 and December 2021 are similar to the costs we found in Sober Look, and performance is similarly poor. We now analyze the relationship between the costs we document in Table 1 and the post-merger returns we document in Table 2. Table 3 presents the results of this analysis, using net cash per share to predict post-merger share prices. This was the central analysis in Sober Look, and is our primary interest here. A strong, positive relationship would imply that the current SPAC crash was predictable.

In Sober Look, we found that while immediate post-merger share prices were positively correlated with pre-merger net cash per share, the correlation grew stronger as post-merger share prices tended to fall for well over a year as the market learned more about a post-merger company’s performance. We find the same dynamic in the SPACs analyzed here. The correlations between pre-merger net cash per share and share prices one day and one week after a merger are positive and statistically significant. Share prices, however, continue falling for months after a merger as the market observes the actual performance of these companies. We therefore measure share prices as of December 1, 2022. We adjust post-merger share prices for changes in the IPO-index, the Nasdaq index, and the Russell 2000 index.4343. We adjust SPAC returns for those of a benchmark as follows: for each SPAC’s current share price (adjusted for dividends and stock splits) as of December 1, 2022, we divide that price by one plus the return of the reference index between the date of a SPAC’s merger and December 1, 2022. For instance, if the relevant reference index has gone up 10% since the time of a SPAC’s merger, and the SPAC’s share price is currently $11, the market adjusted share price would be $11 / 1.1 = $10. We add fixed effects for the month that a deal was closed and the month it was announced. These control for time-varying factors, most notably the SPAC bubble between the last quarter of 2020 and the first quarter of 2021. Pre-merger share prices during the bubble period were well above SPAC redemption prices of about $10.4444. We show this in a postscript to our primary analysis. Sober Look, supra note 1, at 290-98. As a result, shareholders seeking an exit would sell their shares rather than redeeming them. So, redemptions were low, and net cash per share was commensurately higher than in other periods.4545. During the bubble period of the fourth quarter of 2020 and the first quarter of 2021, redemptions averaged 22%, compared to average redemptions of 59% during the prior year and 54% during the subsequent year. As we explained above, redemptions reduce both cash and outstanding shares, but they reduce cash proportionately more, and therefore reduce net cash per share.

In all three models in Table 3, the correlation between net cash per share and post-merger share price is positive and highly significant. In model (1), which uses post-merger prices adjusted for the IPO-index, the coefficient on cash per share is essentially one, matching the results we found in Sober Look and suggesting that SPAC shareholders, on average, bore the entire marginal cost of increases in SPAC dilution. In the other models, using prices adjusted by the Nasdaq and Russell 2000, the coefficients are 0.55 and 0.50, respectively. These coefficients are lower than in Sober Look, but they still indicate that SPAC shareholders bore high SPAC costs. When adjusting post-merger prices by the Nasdaq or Russell 2000, SPAC shareholders received, on average, shares worth less than the cash per share SPACs delivered.4646. The average post-merger share price, when adjusting for changes in the Nasdaq and Russell 2000, is $4.58 and $4.23, respectively, as of December 1, 2022. These share prices are both well below the $6.40 in average cash per share delivered by SPACs. If target companies had traded shares worth $6.40 in exchange for $6.40 in pre-merger net cash, they would have born zero costs from the transaction. The fact that they traded shares worth on average about $4.50 in exchange for $6.40 in pre-merger net cash indicates that they, on average, got very good deals from the SPACs with which they merged. By contrast, SPAC shareholders got shares worth even less than the average cash per share their SPACs delivered. The fact that the coefficients in models (2) and (3) are below one indicates that when adjusting post-merger prices for the Nasdaq or Russell 2000, SPACs with high cash per share did not do as much better compared to SPACs with low cash per share as the results in model (1) suggest. This could be due in part to the high degrees of market volatility and uncertainty in the second half of 2020 and 2021, and thus an increased difficulty on the part of targets in estimating the cash per share SPACs would deliver and in evaluating the value of the shares they were giving up to SPAC shareholders. Overall, we view all of the results in Table 3 as supporting the structural connection between net cash per share and poor returns, though there is now somewhat more complexity to that relationship than we observed in Sober Look.

D. Confounding Factors in Empirically Confirming the Link Between Net Cash Per Share and Post-Merger Share Prices

The relationship between net cash per share and post-merger share price is strong as a logical proposition. As we explain supra Section II.B, however, confirming the relationship empirically encounters two complications. First, deals that the market expects to have higher post-merger share prices will tend to have lower redemptions, which will result in more cash per share. To the extent that a target can anticipate the market’s perception, this is not a problem for our inference, but new information may emerge after the merger agreement is signed that influences redemptions and creates a link between pre-merger net cash per share and post-merger share price that does not depend on a target’s negotiations with the SPAC. Second, SPACs with experienced sponsors with reputations in the market may have higher net cash per share and, for reasons apart from their net cash per share, may achieve higher post-merger value for their shareholders. Neither of these potential causal influences would negate the causal relationship between net cash per share and post-merger returns, but they would affect the interpretation of the results in Table 3.

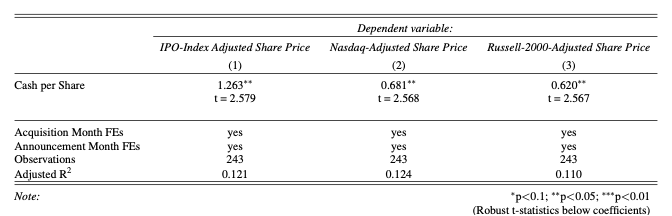

In order to investigate the issue of redemptions as a confounding factor, we re-calculate net cash per share under an assumption of zero redemptions.4747. When computing SPACs’ total pre-merger cash, we assume, counterfactually, that the entire trust amount is still available, and when computing SPACs’ total pre-merger shares, we assume, counterfactually, that no shares were redeemed. All other factors for the cash per share calculation—the sponsor’s promote, warrants, banking fees and PIPE—remain the same. An alternative approach would be to run a regression that predicts post-merger share prices based on both cash per share and redemptions. The problem with this approach, however, is that it would represent a form of “conditioning on the response,” or “overcontrolling.” The reason is that, according to our analyses, deals that have low cash per share (even apart from redemptions) are likely to be worse deals for investors post-merger, and an effect of bad deals is high redemptions. Controlling for a factor (redemptions) that is an effect of one’s main outcome (merger agreements that over-value the target company), would be like studying the impact of a job training program on participants’ employment, while controlling for participants’ income, where income is clearly an effect of the outcome of interest, employment. By computing a “pre-redemption” cash per share, we avoid this difficulty. Ideally, we would only remove redemptions influenced by new information that becomes available after the merger agreement, but since this is not practicable, we perform an even more stringent test by removing the influence of all redemptions. Table 4 presents the results of this analysis and shows that net cash per share is still a statistically significant predictor of post-merger share price. These results confirm that net cash per share is highly correlated with post-merger share price, and that the association is not simply driven by redemptions responding to market perceptions of an announced merger.4848. In other analyses, we remove both redemptions and PIPEs from our cash per share calculations, and reach similar results. Removing PIPEs is an even more overly stringent test of our theory, since PIPE agreements are negotiated simultaneously with the terms of the merger agreement. This means that targets can balance between larger PIPEs and the lower valuations needed to secure them, versus smaller PIPEs and higher valuations, and thereby structure deals in which they expect to receive cash per share that is roughly commensurate with the value they give up. The results of these tests with no PIPE and no redemptions vary depending on which date we use to obtain post-merger prices. As of August 2022, when we first submitted this Essay for publication, the coefficients are 2.457 (t = 2.298**), 1.911 (t = 2.709***) and 1.807 (t = 2.598***) for the analyses that use this counterfactual no-PIPE, no-redemption version of cash per share to predict post-merger value adjusted for the IPO, Nasdaq, and Russell 2000 indices, respectively. When we added the “HQ Control” as in Table 5, the coefficients were 2.181 (t = 1.847*), 1.685 (t = 2.215**) and 1.520 (t = 2.037**) respectively. By the time we finalized this Essay for publication, the data, as of December 1, 2022, had shifted the results of these analyses and the cash per share figures were no longer statistically significant. For instance, in the analysis that counterfactually assumes no redemptions, no PIPE, and adds HQ sponsor controls, the coefficients were 1.24 (t = 0.744), 0.709 (t = 0.781), and 0.598 (t = 0.718) when adjusting post-merger prices according to the IPO index, the Nasdaq, and the Russell 2000. There are two competing influences on our analyses from allowing more time to elapse post-merger. On the one hand, this can allow more time for markets to more accurately value post-merger shares, which should strengthen the relationship between cash per share and post-merger share price. On the other hand, the more time that elapses, the more that idiosyncratic factors can influence the prices of individual companies, thus attenuating the relationship. In this case, the later factor appears to have been stronger, although we note that all of our main results in tables still remain strongly statistically significant, even using data from December 1, 2022.

In order to investigate the second confounding factor, relating to SPAC sponsor quality, we now add a control variable for our “high quality” sponsor designation. If variation in sponsors’ abilities to negotiate attractive mergers is driving the relationship between pre-merger net cash per share and post-merger share price for reasons unrelated to the net cash they deliver, then adding a control for sponsor quality should reduce the predictive ability of net cash per share. Table 5 presents this analysis, showing comparisons of models with and without controls for sponsor quality. Coefficients for the net cash per share variable are quite similar to those in Table 3, as is their statistical significance. In unreported regressions, we replicated the models in Table 5 using the zero-redemption assumption of Table 4 and found little change in coefficients or statistical significance. The quality of a sponsor may still influence the deal struck on behalf of SPAC shareholders (in ways apart from net cash per share) and hence influence post-merger share price, but such a relationship is not borne out in these tests. We also tested different definitions of “high quality,” which yielded similar results.4949. In those regressions, we used the following definitions: (a) affiliation with an investment fund with at least $1 billion AUM; (b) former CEO of a Fortune 500 company; (c) former senior executive (board chair or C-level executive) of a Fortune 500 company and (d) “serial SPAC sponsor” that has completed three or more SPAC mergers. Results are similar regardless of our definition. In other unreported tests, we fit separate models for high-quality sponsors and other sponsors. As in Sober Look, coefficients in those separate models are similar to the coefficients in the models reported in Table 5.5050. For instance, when predicting IPO-adjusted post-merger share price among only high-quality sponsors, cash per share has a coefficient of 0.731 (t = 1.759*), and among non-high-quality sponsors, cash per share has a coefficient of 1.145 (t = 2.891***).

III. Conclusion

The analysis above, using data from the 243 SPACs that merged between July 2020 and December 2021, is consistent with our analysis in Sober Look of the 47 SPACs that merged between January 2019 and June 2020. SPACs’ pre-merger net cash per share continues to be low—though not as low as in the Sober Look cohort—and its correlation with post-merger returns continues to be high. With more observations to work with than we had in Sober Look, we have provided some reassurance that the empirical relationship we see in the data reflects that relationship. As we recognized in Sober Look, our empirical analysis alone cannot prove causation. But the logic behind the link between pre-merger net cash per share and post-merger return is strong. A SPAC merger is a financing transaction for a target. It is, in effect, an offering of the target’s shares to the public. Surely a target focuses on the net cash it will receive for its shares.

So, yes, because SPACs’ structure has remained unchanged, the SPAC crash was predictable.

† Michael Klausner is the Nancy and Charles Munger Professor of Business and Professor of Law, Stanford Law School. Professor Klausner is currently consulting on SPAC-related litigation that relates to the analysis in this Essay.

†† Michael Ohlrogge is an Associate Professor of Law, New York University School of Law. Professor Ohlrogge is currently consulting on SPAC-related litigation that relates to the analysis in this Essay. The authors thank Nikki Bauer, Leo Rassieur, Erica Freeman, and Wenting Tao for their excellent research assistance, and Harald Halbhuber and Jay Ritter for helpful suggestions on an earlier draft.